Reporting entity

Entity (Lender) name: ____________

Fund Manager Organization Name (if applicable): ____________

The GRESB Real Estate Lender Standard and Reference Guide (“Reference Guide”) accompanies the GRESB Real Estate Lender Assessment and is published both as a standalone document and in the GRESB Portal alongside each assessment indicator. The Reference Guide reflects the opinions of GRESB and not of our members. The information in the Reference Guide has been provided in good faith and on an “as is” basis. We take reasonable care to check the accuracy and completeness of the Reference Guide prior to its publication. While we do not anticipate major changes, we reserve the right to make modifications to the Reference Guide. We will publicly announce any such modifications.

The Reference Guide is not provided as the basis for any professional advice or for transactional use. GRESB and its advisors, consultants, and sub‑contractors shall not be responsible or liable for any advice given to third parties, any investment decisions or trading, or any other actions taken by you or by third parties based on information contained in the Reference Guide.

Except where stated otherwise, GRESB is the exclusive owner of all intellectual property rights in all the information contained in the Reference Guide.

The GRESB Real Estate Lender Standard and Reference Guide provides a comprehensive explanation of the reporting requirements for each Indicator of the GRESB Real Estate Lender Assessment. It reflects the structure of the assessment itself, which lenders should complete within the GRESB Assessment Portal.

The Reference Guide is complemented by the Scoring Document, which explains each Indicator’s scoring methodology. Together, these documents help GRESB Lenders understand the assessment criteria, meet reporting requirements, and interpret their scores effectively.

For more information about GRESB, please contact info@helpdesk.gresb.com.

For additional guidance in completing the assessment and interpreting its results, refer to Appendix 2.

The GRESB Lender Assessment empowers real estate lenders to efficiently evaluate their internal ESG capabilities and programs, ensuring effective management of related risks and impacts. Through a consistent framework and actionable insights, the assessment helps lenders align with sustainability goals and make more informed decisions regarding their loan portfolio and investments.

The methodology is consistent across different regions, lending programs, and investment vehicles, and aligns with international reporting frameworks, such as the Task Force on Climate-Related Financial Disclosures (TCFD), Global Reporting Initiative (GRI), and Principles for Responsible Investment (PRI).

The Real Estate Lender Assessment generates the GRESB Real Estate Lender Benchmark, which is structured into two (2) distinct components, namely the Management- and Performance Component.

Each Indicator in the assessment is allocated to one of the three sustainability dimensions (E‑ environmental; S‑ social; G‑ governance):

| E | S | G | |

|---|---|---|---|

| Management | 21% | 12% | 67% |

| Performance | 100% | 0% | 0% |

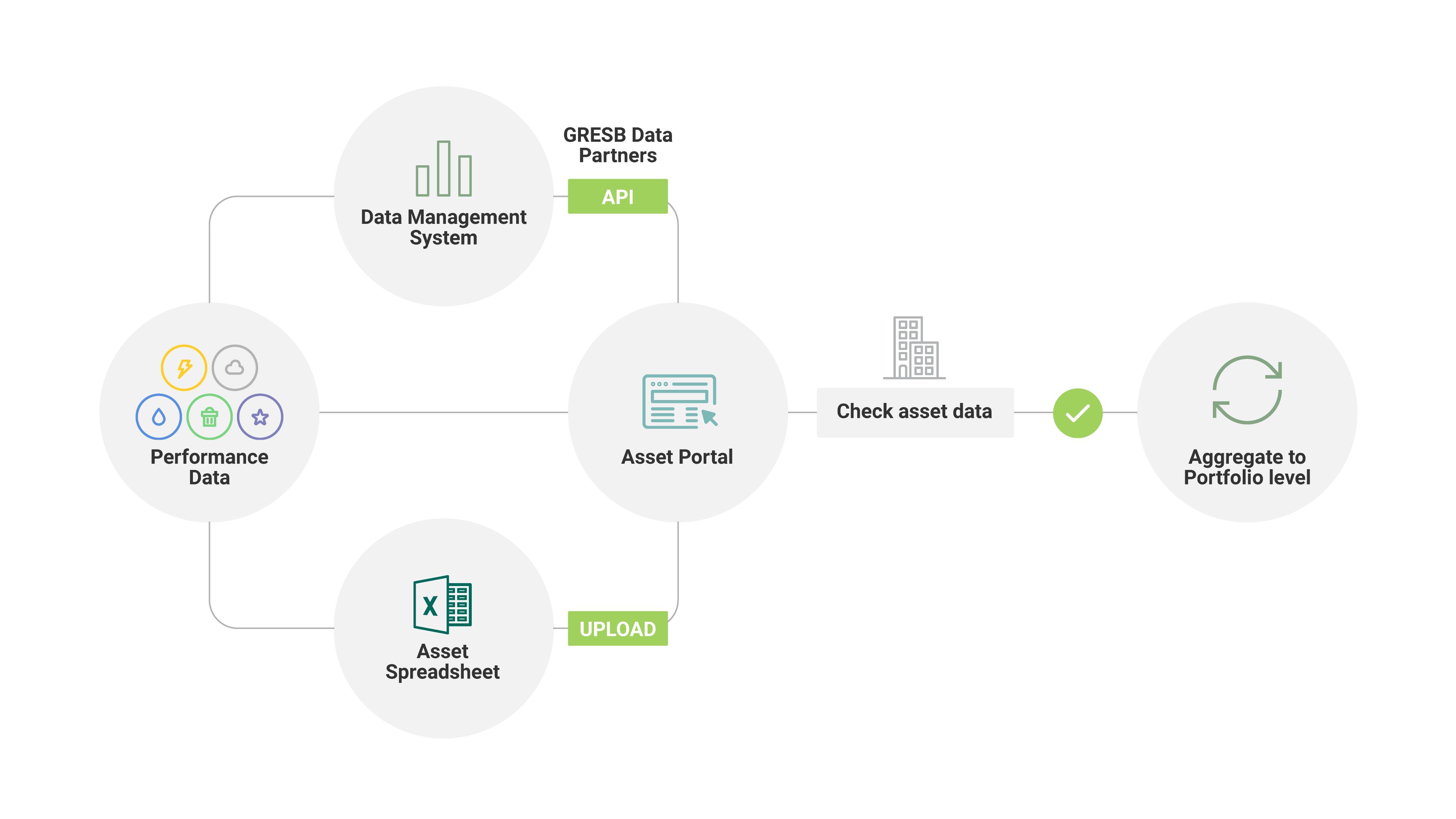

Each Indicator is identified by a short title (e.g. ESG Objectives) and a code (e.g. LLE1). All Indicators include a primary question that can be answered with ‘Yes,’ ‘No,’ or 'Not Applicable'. The Energy, GHG and Building Certifications Indicators in the Performance Component are answered with asset-level data, which may be reported through the Asset Spreadsheet or the asset workspace in the GRESB Portal (referred to as the “Asset Portal”).

The General Feedback section consists of several open text boxes. Lenders are encouraged to offer feedback, as this informs future advances to the GRESB Lender Standard.

Scoring details can be found in the Scoring Document.

Response types for each Indicator may use one or more of the following elements:

The GRESB Real Estate Lender Assessment provides lenders with actionable information and tools to monitor and manage the sustainability-related risks and opportunities of their loans and to prepare for increasingly rigorous ESG-related obligations.

GRESB Real Estate Lender Benchmark Members receive comparative business intelligence on where they stand against their peers, a roadmap with the actions they can take to improve their ESG performance, and a communication platform to engage with investors.

Lenders who submit the Real Estate Lender Assessment will receive a Benchmark Report.

The Assessment Portal opens on Tuesday April 1. The submission deadline is Friday August 1 (23:59:59 PST), providing lenders with a four‑month window to complete the assessment.

GRESB releases the final results to each individual GRESB Lender Benchmark Member on October 1, 2025.

GRESB requires lenders to report on their whole loan portfolio for the Performance Component. This includes all real estate loans that were held during the prior year, including those that originated, matured or sold (e.g., through a securitization).

Lenders must report on all loans that were part of their loan portfolio during the prior year. However, loans backed by vacant land, dormant assets, ground lease, or other non–real estate assets may be excluded from this requirement.

A "dormant asset" is defined as a property that is entirely non-operational during the reporting period and, as such, neither consumes energy or water nor generates emissions or waste. This designation applies primarily to assets marked for major redevelopment or similar inactive status. Assets consuming residual resources, such as standby energy for minimal operations, do not qualify as dormant and must be included in the Performance Component. The dormant classification applies strictly to assets without any operational activity or resource use.

Building utilities often have different spans of control, landlord responsibility vs tenant responsibility, driven by varying lease structures. GRESB differentiates between landlord-controlled and tenant-controlled areas in the Energy and GHG Emissions aspects of the Performance Component. Lenders in the Real Estate Lender Assessment can report building data for assets in their loan portfolio using the Asset Spreadsheet and/or the Asset Portal. In most cases, borrowers serve as the landlords, and GRESB acknowledges that landlords of tenant-controlled areas often have limited or no control over utility consumption, procurement, or waste management practices at the asset level. GRESB encourages lenders to seek whole building data from its borrowers, regardless of span of control.

GRESB does not specifically distinguish between landlord- and tenant-controlled areas outside of the Energy, and GHG Emissions.

Information provided in the Entity and Reporting Characteristics aspect identifies the reporting entity's characteristics that remain constant across different reporting years.

EC1

Reporting entity

Entity (Lender) name: ____________

Fund Manager Organization Name (if applicable): ____________

Identify the participating entity. This information will be displayed in the GRESB Portal and in the entity’s Benchmark Report(s).

Complete all applicable fields.

Entity manager (organization) name: Legal name of the organization that manages the entity (typically applicable for non-listed entities only).

Entity name: Fund or company name of the entity for which the Assessment is submitted. In the case of listed companies, the entity name is the legal name of the organization, also used for identification on international stock exchanges. In the case of non-listed entities, the entity name identifies the portfolio for which the Assessment is submitted.

LEC2

Nature of ownership

Public (listed on a Stock Exchange) entity / lender

Specify ISIN: ____________

Type:

Bank

Insurance Company

Mortgage Real Estate Investment Trust (mREIT)

Other

Specify the type: ____________

Dominant Lending style (by % of loan portfolio in reported currency):

Senior Debt

Subordinated Debt

Unitranche Debt

Other

Specify the dominant lending style: ____________

Private (non-listed) entity / lender

Type:

Bank

Club Deal

Fund

Insurance Company

Joint Venture (JV)

Separate Account

Special Purpose Vehicle

Other

Specify the type: ____________

Dominant Lending style (by % of loan portfolio in reported currency):

Senior Debt

Subordinated Debt

Unitranche Debt

Other

Specify the dominant lending style: ____________

Describe the real estate lender type and nature of the participating entity. Participants should select the most applicable type that fits the reporting entity. This criteria may be used for peer benchmarking purposes.

Select one of the options and select all applicable sub-options.

If two or more listed companies merge into one entity during the reporting year, report on the structure, policies and procedures of the newly formed entity as of the end of the reporting year.

Public entity: A company that is publicly listed and traded on a recognized stock exchange, such as Nasdaq or NYSE. Also known as "listed entities”.

ISIN: International Securities Identification Number. ISINs are assigned to securities to facilitate unambiguous clearing and settlement procedures. They are composed of a 12-digit alphanumeric code and act to unify different ticker symbols, which can vary by exchange and currency for the same security. In the United States, ISINs are extended versions of 9-character CUSIP codes.

Private entity: A company or fund that is not a listed or traded on any stock exchange. Also known as a non-listed entity.

mREIT: A Mortgage Real Estate Investment Trust is a specialized financial vehicle that provide funding for real estate through the purchase of mortgages and mortgage-backed securities. Listed mREITs are traded on a stock exchange.

Senior Debt: A form of debt financing that holds the highest claim on a borrower’s assets in the event of default or liquidation. Typically secured and lower in risk, it carries lower yields compared to other debt forms.

Subordinated Debt: Debt that ranks below senior debt in the repayment hierarchy. In a default scenario, subordinated debt is repaid only after all senior obligations have been satisfied, resulting in higher interest rates to compensate for the increased risk.

Unitranche Debt: A hybrid financing structure that combines both senior and subordinated debt into a single loan facility. This approach simplifies capital arrangements by providing one blended interest rate and consolidated terms reflective of the overall risk profile.

Club Deal An investment vehicle or structure with generally a limited number of investors investing in a common strategy. Typically, investors have more discretion and control than in a typical fund, and have veto rights over major decisions.

Fund or vehicle: Terms used to describe a structure where at least three investors’ capital is pooled together and managed as a single entity with a common investment aim. For the purposes of these definitions, these terms can be used interchangeably.

Joint Venture: A vehicle where at least two parties share a common investment objective. Control over significant risk management decisions is not transferred to an external manager, but is exercised by members in the venture.

Separate Account: SMAs, also referred to as managed accounts, wrap accounts or individually managed accounts, are portfolios managed exclusively for the investor according to their investing and tax preferences and requirements.

Special Purpose Vehicle Subsidiary created by a parent company to isolate financial risk. Its legal status is of a separate company, with its own balance sheet.

Other: Answers provided under 'Other' must be outside the options listed in the indicator to be valid.EC3

Entity / Lender commencement date

Year of commencement (listed) or Year of establishment (non-listed)

________________________

Describe the activity year of commencement or establishment date of the entity.

Provide the year of commencement/establishment.

Year of commencement: The year in which the reporting entity began investing in the market. If a listed entity is delisted (i.e., taken private) but remains under the same management, the date of original commencement can be used for “date of first closing” for the new non-listed entity. If the entity is taken private by a new management company, the first day of closing should be the date of privatization. This information is not used for scoring and used for context only; portfolio vintage may affect the ability to implement ESG policies and strategies.

Year of establishment: A date specified by the manager on which the vehicle is launched, the initial capital subscription is completed, and the commitment period commences.

EC4

Reporting year

Calendar year

Fiscal year

Specify the starting month Month

Set the entity’s annual reporting year.

Select one of the options.

Participants are required to specify the starting month of their fiscal year. If participants select Fiscal year, starting months between February and June must correspond to calendar years 2024/2025. For example, an entity reporting from April to March will be considered covering the period of April 2024 - March 2025. On the other hand, starting months between July and December must correspond to calendar years 2023/2024. For example an entity reporting from October to September will be considered as covering the period of October 2023 - September 2024.

The table below details the period for which information throughout the Assessment would be expected, should a given starting month be selected:

| Starting month | Reporting Year |

|---|---|

| January | Select "Calendar Year" |

| February | Feb 2024 - Jan 2025 |

| March | Mar 2024 - Feb 2025 |

| April | Apr 2024 - Mar 2025 |

| May | May 2024 - Apr 2025 |

| June | Jun 2024 - May 2025 |

| July | Jul 2023 - Jun 2024 |

| August | Aug 2023 - Jul 2024 |

| September | Sept 2023 - Aug 2024 |

| October | Oct 2023 - Sept 2024 |

| November | Nov 2023 - Oct 2024 |

| December | Dec 2023 - Nov 2024 |

Calendar year: January 1 – December 31.

Fiscal year: The period used to calculate annual financial statements. Depending on the jurisdiction the fiscal year can start on April 1, July 1, October 1, etc.

Reporting year: Responses provided in the Assessment must refer to the reporting year identified in this indicator and should correspond to the most recently closed calendar year / fiscal year, as applicable. A response to an indicator must be true at the close of the reporting year; however, the response does not need to have been true for the entire reporting year. GRESB does not favour the use of calendar year over fiscal year or vice versa, as long as the chosen reporting year is used consistently throughout the Assessment.

LEC5

Nature of the business

Loan originator

Percentage of originations held on balance sheet: ____________%

Percentage of originations held on balance sheet - Green- / Social loans

________________________%

Percentage of originations held on balance sheet - Sustainability-Linked Loans

________________________%

Percentage of originations syndicated: ____________%

Percentage of originations syndicated - Green- / Social loans

________________________%

Percentage of originations syndicated - Sustainability-Linked Loans

________________________%

Percentage of originations securitized: ____________%

Percentage of originations securitized - Green- / Social loans

________________________%

Percentage of originations securitized - Sustainability-Linked Loans

________________________%

Loan purchaser

Percentage of portfolio purchased: ____________%

Percentage of portfolio purchased - Green- / Social loans

________________________%

Percentage of portfolio purchased - Sustainability-Linked Loans

________________________%

Describe the nature of the participating entity’s business. Participants should select the applicable answer and provide percentages per loan type.

Complete all applicable fields.

Participants must provide portfolio split per sub-category at the end of reporting period.

Note: Sum of reported percentages should not exceed 100%.

Loan originator: The lender that serves as the primary loan underwriter and provides proceeds to the borrower.

Loan purchaser: The party that purchases a loan or group of loans from a loan originator.

Securitized loan: Type of loan where multiple loans are pooled together, consolidated, and sold in tranches with specific payment and risk characteristics.

Syndicated loan: A large loan arranged by a group of international banks that form a syndicate, headed by a lead manager.

Green- / Social Loans: Financing facilities in which the use of proceeds is exclusively dedicated to projects with specific environmental and/or social objectives. These loans support initiatives such as renewable energy, energy efficiency improvements, affordable housing, the presence or attainment of building certifications or other projects that generate measurable ESG benefits.

Sustainability-Linked Loans: A form of financing where the loan terms, including the interest rate, are linked to the borrower’s achievement of predetermined sustainability or ESG performance targets. Should the borrower meet or exceed these targets, they may benefit from reduced borrowing costs or other favorable terms. This structure is designed to incentivize continuous improvement in sustainability performance while aligning financial benefits with responsible business practices.

RC1

Reporting currency

Values are reported in: Currency

Set the currency for which the entity’s real estate portfolio of loans is denominated.

State the currency used by the entity for Assessment indicators that require a monetary value as a response.

Other: State the other currency form.

RC2

Economic size

What is the aggregate unpaid principal balance (i.e. outstanding loan value) of the entity's portfolio at the end of the reporting year in millions?

________________________

State the size of the entity. Participants should report aggregate unpaid principal balance (UPB) due to the entity at the end of the reporting period.

UPB: The unpaid portfolio balance is the total outstanding loan value of the entity’s portfolio at the end of the reporting period.

Unpaid principal balance (UPB) is a metric used in GRESB data analysis to identify the size of the reported portfolio.

Complete the value in millions using the designated field (e.g. UPB of $75,000,000 must be reported as 75).

Do not write the currency, as this has been selected in Indicator RC1.

RC3

Floor area metrics

Metrics are reported in:

m2

sq. ft.

Metrics are needed to ensure comparability for reporting purposes. Set the reporting units used by the entity.

Select one of the options, and use it consistently when reporting the floor area of the portfolio.

RC4

Property type and Geography

Portfolio predominant location: Location

Provide information on the entity's portfolio location. This indicator is used for reporting purposes only.

Select the predominant location in which the entity’s loans are located using the fraction of total unpaid principal balance. In order to select a location, at least 60% of the unpaid principal balance should be allocated to that location.

Note: The predominant country drop-down menu includes less granular options, such as sub-regions, regions, and "Globally Diversified".

EPRA Best Practices Recommendations on Sustainability Reporting, 3rd version, September 2017: 5.7, Analysis-Segmental-Analysis

Management: Leadership

Management: LeadershipThis section evaluates how the entity integrates ESG into its overall business strategy. The purpose of this section is to (1) identify public ESG commitments made by the entity, (2 & 3) assess the establishment of ESG objectives and the actions taken to achieve them, (4) identify who is responsible for ESG and climate-related decision-making, and (5) evaluate the presence of ESG performance targets for personnel to ensure accountability in sustainability efforts.

LLE1

ESG leadership commitments

Has the lender made a public commitment to ESG leadership standards and/or principles?

Yes

Select all commitments included (multiple answers possible)

General ESG commitments

Global Investor Coalition on Climate Change (including AIGCC, Ceres, IGCC, IIGCC)

International Labour Organization (ILO) Standards

Multifamily Impact Framework

OECD - Guidelines for multinational enterprises

PRI signatory

RE 100

Science Based Targets initiative

Task Force on Climate-related Financial Disclosures (TCFD)

UN Environment Programme Finance Initiative

UN Global Compact

UN Sustainable Development Goals

CERES Ambition 2030

Canadian Investor Statement on Climate Change

Other: ____________

Provide applicable hyperlink

URL____________

Indicate where in the evidence the relevant information can be found____

Net Zero commitments

Net Zero Banking Alliance

Net Zero Insurance Alliance

GFANZ

Science Based Targets initiative: Net Zero Standard commitment

The Climate Pledge

Transform to Net Zero

ULI Greenprint Net Zero Carbon Operations Goal

UNFCCC Climate Neutral Now Pledge

WorldGBC Net Zero Carbon Buildings Commitment

CERES Ambition 2030

Other: ____________

Provide applicable hyperlink

URL____________

Indicate where in the evidence the relevant information can be found____

No

LE1

1 point , G

This indicator assesses the entity's commitment to ESG leadership standards or principles. By making a commitment to ESG leadership standards or principles, an entity publicly demonstrates its commitment to ESG, uses organizational standards and/or frameworks that are universally accepted and may have obligations to comply with the standards and/or frameworks.

Select yes or no. If yes, select all applicable sub-options.

URL: Hyperlink is mandatory for this indicator, but is used for reporting purposes only. Ensure that the hyperlink is not outdated and the relevant page can be accessed within two steps. The URL should demonstrate the existence of publicly available commitments to ESG/Net Zero leadership relating to each of the standards and/or principles selected.

Other: State the other public commitment. Ensure that the other answer provided is not a duplicate of a selected option above. It is possible to report multiple other answers.

This indicator is not subject to automatic or manual validation.

See Appendix 3 - Validation for additional information about GRESB Validation.

1 point, G

Scoring is based on the number of selected options. It is not necessary to select all options to achieve the maximum score.

See the Scoring Document for additional information on scoring.

Canadian Investor Statement on Climate Change: The Canadian Investor Statement on Climate Change is a commitment by institutional investors to support the transition to a net-zero economy by 2050. Signatories pledge to integrate climate considerations into investment decisions, engage with companies on climate-related risks, and advocate for policies that align with the Paris Agreement.

ESG leadership standards and/or principles: International governmental or organizational standards, principles, frameworks, and/or initiatives that are universally accepted and include a public commitment (i.e., via a public register). These standards are governed independently from commercial interests of one or multiple groups. They are defined in alignment with international frameworks of advancing ESG with accountability and obligations to comply with the standards.

Global Investor Coalition on Climate Change: A collaboration among four regional partner organisations around the world to increase investor education and engagement on climate change and climate-related policies. Launched in 2012, the coalition provides a global platform for dialogue between and among investors and world governments to accelerate low-carbon investment practices, corporate actions on climate risk and opportunities, and international policies that support the goals of the Paris Agreement.

International Labour Organization (ILO) Standards: International labour standards are legal instruments drawn up by the ILO's constituents (governments, employers and workers) and setting out basic principles and rights at work.

Multifamily Impact Framework: A market-based, common framework of industry impact principles and reporting guidelines for multifamily properties in the United States.

Net Zero leadership standards and/or principles: International governmental or organizational standards, principles, frameworks, and/or initiatives that are universally accepted and include a public commitment (i.e., via a public register). These standards are governed independently from commercial interests of one or multiple groups. They are defined in alignment with international frameworks on Net Zero with accountability and obligations to comply with the standards.

OECD - Guidelines for multinational enterprises: The OECD Guidelines for Multinational Enterprises are recommendations addressed by governments to multinational enterprises operating in or from adhering countries. They provide non-binding principles and standards for responsible business conduct in a global context consistent with applicable laws and internationally recognised standards.

PRI: The PRI works with its international network of signatories to put the six Principles for Responsible Investment into practice. Its goals are to understand the investment implications of environmental, social and governance issues and to support signatories in integrating these issues into investment and ownership decisions.

RE 100: RE100 is a global initiative uniting businesses committed to 100% renewable electricity, working to massively increase demand for and delivery of renewable energy. RE100 is convened by The Climate Group in partnership with CDP.

Science Based Targets initiative: The initiative is a collaboration between CDP, the United Nations Global Compact, World Resources Institute, and the World Wide Fund for Nature (WWF) which has a goal of enabling companies setting science based targets to reduce GHG emissions.

Science Based Targets initiative - Net Zero Standard commitment: The SBTi’s Corporate Net-Zero Standard is a framework for corporate net-zero target setting in line with climate science. It includes the guidance, criteria, and recommendations companies need to set science-based net-zero targets consistent with limiting global temperature rise to 1.5°C.

Task Force on Climate-related Financial Disclosures (TCFD): The Task Force on Climate-related Financial Disclosures will develop voluntary, consistent climate-related financial risk disclosures for use by companies in providing information to investors, lenders, insurers, and other stakeholders.

The Climate Pledge: The Climate Pledge is a commitment to reach net-zero carbon emissions by 2040—10 years ahead of the Paris Agreement.

Transform to Net Zero: Transform to Net Zero aims to deliver guidance and business plans to enable a transformation to net zero emissions, as well as research, advocacy, and best practices to make it easier for the private sector to not only set ambitious goals–but also deliver meaningful emissions reductions and economic success.

ULI Greenprint Net Zero Carbon Operations Goal: The ULI Greenprint goal is to reduce the carbon emissions of its members' collective buildings under operational control to net zero by the year 2050.

UN Environment Programme Finance Initiative: The UNEP FI is a partnership between United Nations Environment and the global financial sector with a mission to promote sustainable finance.

UN Global Compact: The UN Global Compact is a voluntary initiative based on CEO commitments to implement universal sustainability principles and to take steps to support UN goals.

UN Sustainable Development Goals: The Sustainable Development Goals are a universal call to action to end poverty, protect the planet and improve the lives and prospects of everyone, everywhere. The 17 Goals were adopted by all UN Member States in 2015, as part of the 2030 Agenda for Sustainable Development which set out a 15-year plan to achieve the Goals.

UNFCCC Climate Neutral Now Pledge: Climate Neutral Now encourages and supports organizations and other interested stakeholders to act now in order to achieve a climate neutral world by 2050 as enshrined in the Paris Agreement.

WorldGBC’s Net Zero Carbon Buildings Commitment: The Net Zero Carbon Buildings Commitment (the Commitment) challenges companies, cities, states and regions to reach Net Zero operating emissions in their portfolios by 2030, and to advocate for all buildings to be Net Zero in operation by 2050.

Canadian Investor Statement on Climate Change

International Labour Organization, International Labour Organization Standards, 2014

Net Zero Asset Managers initiative

OECD Guidelines for Multinational Enterprises

PAII Net Zero Asset Owner Commitment

Science Based Targets initiative

Task Force on Climate-related Financial Disclosures, 2015

ULI Greenprint Net Zero Carbon Operations Goal

UN Global Compact Principles, 2000

UN Sustainable Development Goals

UN-convened Net-Zero Asset Owner Alliance

UNEP Finance Initiative Statement, 1992

LLE2

ESG objectives

Does the lender have ESG objectives?

Yes

The objectives relate to (multiple answers possible)

General objectives

Environment

Social

Governance

Issue-specific objectives

Energy efficiency

Health and well-being

Resilience

Other: ____________

The objectives are

Publicly available

Provide applicable hyperlink

URL____________

Indicate where in the evidence the relevant information can be found____

Not publicly available

Communicate the objectives and explain how they are integrated into the overall business strategy (maximum 250 words)

________________________

No

LE2

2 points , G

Clear Environmental, Social, and Governance (ESG) objectives help participants identify material issues and integrate them into the overall day-to-day management practices.

Select yes or no. If yes, select all applicable sub-options.

URL: Hyperlink is mandatory for this indicator when publicly available is selected, but is used for reporting purposes only. Ensure that the hyperlink is not outdated and the relevant page can be accessed within two steps. The URL should demonstrate the existence of publicly available ESG objectives for each of the objectives selected.

Open text box: The content of this open text box is not used for scoring, but will be included in the Benchmark Report. Participants should use this open text box to communicate on

This indicator is not subject to automatic or manual validation.

See Appendix 3 - Validation for additional information about GRESB Validation.

2 points, G

Scoring is based on the number of selected options. It is not necessary to select all options to achieve the maximum score.

Open text box: The open text box is not scored and is for reporting purposes only.

See the Scoring Document for additional information on scoring.

Energy efficiency: Refers to products or systems using less energy to provide the same consumer benefit.

Environmental objectives: Overall goals arising from policies that an entity sets itself to achieve regarding relevant environmental issues, such as greenhouse gas emissions, renewable energy, or sustainable procurement. These objectives should be quantifiable and correlated with the entity's ambitions. The objectives should be quantifiable and correlated with the entity's ambitions. In turn, they determine targets, which are detailed performance requirements necessary to achieve the environmental objectives.

ESG objectives: Strategic priorities and key topics for the management and/or improvement of ESG issues.

Governance objectives: Overall goals arising from policies that an entity sets itself to achieve regarding relevant governance issues, such as bribery and corruption, cybersecurity, or board composition. These objectives should be quantifiable and correlated with the entity's ambitions.

Health and well-being: “Health is a complete state of physical, mental and social well-being, not merely the absence of disease or infirmity” (WHO). Health & well-being is impacted by genetics and individual behavior as well as environmental conditions. Particularly relevant to GRESB stakeholders are the social determinants of health, which are the “conditions in which people are born, grow, work, live and age, and the wider set of forces and systems shaping the conditions of daily life.” These are the conditions that enable or discourage healthy living. This could include issues such as physical activity, healthy eating, equitable workplaces, maternity and paternity leave, access to healthcare, reduction in toxic exposures, etc.

Resilience: Preparedness of the built environment towards existing and future climate changes (i.e., the ability to absorb disturbances such as increased precipitation or flooding while maintaining its structure). This can be achieved by management policies, informational technologies, educating tenant, community, suppliers and physical measures at the asset level.

Social objectives: Overall goals arising from policies that an entity sets itself to achieve regarding relevant social issues, such as customer satisfaction, employee engagement, or stakeholder relations. These objectives should be quantifiable and correlated with the entity's ambitions.

EPRA Best Practices Recommendations on Sustainability Reporting, 3rd version, September 2017: 5.7, Analysis

SASB (March 2016)-Real Estate Owners, Developers & Investment Trusts: IF0402-05

LLE3

Does the lender take specific steps to achieve the sustainability objectives reported in LLE2?

Yes

Select all applicable actions:

Derive an impact analysis of new construction/major renovation

Formulate borrower's sustainability profile

Provide dedicated financing for sustainability-based property improvements

Engage borrower regarding underperforming assets

Enforce external ESG standards, energy ratings, building certifications, etc.

Analyse long-term sustainability risks of the lending portfolio

Monitor and review asset-level consumption data

Track asset-level sustainability KPIs

Use energy / water / waste metrics as a loan sub-condition

Other: ____________

Describe the process and metrics used to track successful implementation (maximum 250 words)

________________________

No

LLE3

3 points , G

Indicate actions that participant takes to achieve sustainability objectives in LLE2. Participants must select actions that were in-place during the reporting period. Additional context on implementation and tracking actions must be included.

Select yes or no. If yes, select all applicable sub-options.

Open text box: Description provided should fully support each checkbox selected, along with the following elements:

State actions that participant takes to achieve sustainability objectives. These actions must be related to commercial real estate lending.

Other: State the action that participant takes to achieve sustainability objectives in LLE2. Ensure that the other answer provided is not a duplicate of a selected option above. It is possible to report multiple other answers. If multiple other answers are acceptable, only one will be counted towards scoring

See Appendix 3 - Validation for additional information about GRESB Validation.

3 points, G

Scoring is based on the number of selected options. It is not necessary to select all options to achieve the maximum score.

Other: The 'Other' answer is manually validated and points are contingent on the validation decision.

See the Scoring Document for additional information on scoring.

Asset-level consumption data: information regarding energy/water/waste use intensities and overall efficiency of an asset.

External ESG standard: Refers to third party guidance/standards that focuses on ESG integration/management.

Financing for property improvements: Refers to dedicated financing for borrower activities to alter/improve existing buildings. May include major renovation and retrofit.

Impact analysis of new construction/major renovation: Process of identifying the potential consequence of new development and/or alterations to existing asset that affects more than 50 percent of the building floor area.

Standalone sustainable lending policy: Policy or guidance document that outlines real estate lending criteria and includes sustainability-related metrics/factors.

Sustainability commitment: Long and/or short term aims connected to specific metrics/impacts made by the lender.

Sustainability profile: A report/scorecard that includes information about economic, environmental and governance performance and commitments of the borrower.

LLE4

ESG and climate-related decision maker

Does the lender have a decision-maker accountable for ESG and/or climate-related issues?

Yes

ESG

Provide the details for the most senior decision-maker on ESG issues

Name: ____________

Job title: ____________

The individual’s most senior role is as part of

Board of Directors

C-suite level staff/Senior management

Investment Committee

Fund/portfolio managers

Other: ____________

Climate-related risks and opportunities

Provide the details for the most senior decision-maker on climate-related issues

Name: ____________

Job title: ____________

The individual’s most senior role is as part of

Board of Directors

C-suite level staff/Senior management

Investment Committee

Fund/portfolio managers

Other: ____________

Describe the accountability and reporting mechanisms applicable to the most senior decision-maker on ESG and/or climate-related performance of the loan portfolio (maximum 250 words)

________________________

No

LLE4

2 points , G

The presence of senior management dedicated to ESG and/or climate-related risks and opportunities, increases the likelihood that objectives on these topics will be met. A structured process to keep the most senior decision-maker informed on the entity’s ESG/climate-related performance increases accountability and encourages continuous improvement.

Select yes or no. If yes, select the applicable sub-option.

Senior decision-maker: The entity’s most senior decision-maker on ESG and climate is expected to be actively involved in the process of defining the ESG and climate related objectives, and should approve associated strategic decisions regarding ESG and climate.

Details of employee: Participants must provide the name and job title of the relevant employee. This information will be used for reporting purposes only.

Open text box: The content of this open text box is not used for scoring, but will be included in the Benchmark Report. Participants should use this open text box to communicate on

Other: State the other senior decision-maker on sustainability issues. The answer should only refer to the department or governance structure of which the senior decision maker is part of. Ensure that the other answer provided is not a duplicate of a selected option above. Report only one other answer. Note that Fund/Portfolio manager cannot be used as an ‘Other’ answer unless a written statement is included in the open text box confirming that the individual is a senior member.

See Appendix 3 - Validation for additional information about GRESB Validation.

2 points, G

Scoring of this indicator is equal to the fraction assigned to the selected option, multiplied by the total score of the indicator.

Other: The 'Other' answer is manually validated and points are contingent on the validation decision.

Open text box: The open text box is not scored and is for reporting purposes only.

See the Scoring Document for additional information on scoring.

Board of Directors: A body of elected or appointed members who jointly oversee the activities of a company or organization as detailed in the corporate charter. Boards normally comprise both executive and non-executive directors.

C-suite level staff/Senior management: A team of individuals who have the day-to-day responsibility of managing the entity. C-suite level staff are sometimes referred to, within corporations, as senior management, executive management, executive leadership team, top management, upper management, higher management, or simply seniors.

Fund/portfolio manager: A person or a group who manages a portfolio of real estate loans, and the deployment of investor capital, by creating and implementing asset (loan) level strategies, across the entire portfolio.

Board of Directors: A body of elected or appointed members who jointly oversee the activities of a company or organization as detailed in the corporate charter. Boards normally comprise both executive and non-executive directors.

Person accountable: A person with sign off (approval) authority over the deliverable task, project or strategy. The accountable person can delegate the work to other responsible people who will work on the implementation and completion of the task, project or strategy.

Senior decision-maker accountable for climate-related issues: A senior individual with sign off (approval) authority for approving strategic climate-related objectives and steps undertaken to achieve these objectives. The accountable person can delegate the work to other responsible people who will work on the implementation and completion of the task, project or strategy.

Senior decision-maker accountable for ESG: A senior individual with sign off (approval) authority for approving strategic ESG objectives and steps undertaken to achieve these objectives. The accountable person can delegate the work to other responsible people who will work on the implementation and completion of the task, project or strategy.

CDP, CC1.1

GRI Sustainability Reporting Standards (2016): 103-32

RobecoSAM Corporate Sustainability Assessment 2017: 3.1.5, Responsibilities & Committees

Recommendations of the Task Force on Climate-Related Financial Disclosures June 2017: Governance A&B

LLE5

Personnel ESG performance targets

Does the lender include ESG factors in the annual performance targets of personnel?

Yes

Does performance on these targets have predetermined financial consequences?

Yes

Select the personnel to whom these factors apply (multiple answers possible):

Board of Directors

C-suite level staff/Senior management

Investment Committee

Fund/portfolio managers

ESG portfolio manager

Investment analysts

Dedicated staff on ESG issues

External managers or service providers

Investor relations

Other: ____________

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

No

No

LLE5

2 points , G

This indicator identifies whether, and how, ESG issues are addressed in personnel performance targets. It also identifies how the ESG-related objectives outlined in LLE2 are reflected within the organizational structure. Including ESG factors in annual performance targets for employees can increase the entity’s capacity to improve ESG performance.

Select yes or no. If yes, select all applicable sub-options.

If the targets and consequences apply to all employees of the entity, select all relevant personnel types in the indicator.

The provided evidence must cover all the following elements:

Existence of ESG-related performance targets: the evidence must demonstrate that annual ESG performance targets are explicitly tied to the selected personnel groups.

Personnel group applicability: targets must relate to all members within the selected personnel groups.

Financial consequences tied to ESG performance: the evidence must explain the financial implications (positive or negative) for meeting or failing to meet ESG targets for each selected personnel group. This includes clearly linking the financial consequences (e.g., bonuses, pay adjustments, penalties, etc.) to the ESG targets of each selected personnel group. The connection must be clearly defined within the provided documents, open text box, or cover page.

Examples of acceptable evidence: policy documents, process guidelines, employee performance reviews for the reporting year, employment contracts or documentation describing financial consequences (e.g., bonus schemes, web pages). Note that sensitive information may be redacted from the documents as long as the requirements outlined above are clearly met. If the consequences are not clearly defined and connected to the ESG targets within the provided evidence, then sufficient explanation must be provided within the evidence open text box.

Other answers: state the specific employee type and ensure the following:

See Appendix 3 - Validation for additional information about GRESB Validation.

2 points, G

Scoring is based on the number of selected options. It is not necessary to select all options to achieve the maximum score.

Evidence: The evidence is manually validated and points are contingent on the validation decision.

Other: The 'Other' answer is manually validated and points are contingent on the validation decision.

See the Scoring Document for additional information on scoring.

Annual performance targets: Targets set in annual performance reviews, which are assessments of employee performance.

Board of Directors: A body of elected or appointed members who jointly oversee the activities of a company or organization as detailed in the corporate charter. Boards normally comprise both executive and non-executive directors.

C-suite level staff/Senior management: A team of individuals who have the day-to-day responsibility of managing the entity. C-suite level staff are sometimes referred to, within corporations, as senior management, executive management, executive leadership team, top management, upper management, higher management, or simply seniors.

Dedicated staff on ESG issues: Individuals whose core responsibility is to address ESG issues.

ESG portfolio manager: A person or a group who manages the ESG strategy and implementation of a portfolio of real estate investments.

ESG Factors: Criteria associated with the entity’s ESG objectives.

External managers or service providers: Organizations, businesses or individuals that offer services to others in exchange for payment. These include, but are not limited to, consultants, agents and brokers.

Financial consequences: Predetermined monetary benefits (or detriments) incorporated into the employee compensation structures. Examples include bonuses, raises, profit-sharing, financial rewards, and financial incentives. The financial consequences are contingent upon the achievement of the annual performance targets.

Fund/portfolio manager: A person or a group who manages a portfolio of real estate investments, and the deployment of investor capital, by creating and implementing asset level strategies, across the entire portfolio.

Investment analysts: A person or group with expertise in evaluating financial and investment information, typically for the purpose of making buy, sell and hold recommendations for securities.

Investment committee: A group of selected people who establish a formal process to manage the plan’s investment strategy.

Investor relations: A person or a group that provides investors with an accurate account of company affairs so investors can make better informed decisions.

RobecoSAM Corporate Sustainability Assessment 2017: 3.1.7, Executive Compensation-Success Metrics and Vesting

Management: Policies

Management: PoliciesThis aspect confirms the existence and scope of the entity’s policies that address environmental, social and governance issues.

LPO1

Is there a guidance document that describes how sustainability is incorporated into commercial real estate lending?

Yes

Select applicable level

Generalized document that outlines overall approach

Guidance that includes specific sustainability aspects/criteria

Stand-alone policy describing sustainability approach to lending

Policy is applicable during:

Initial loan screening

Collateral assessment

Loan approval process

Post-close loan monitoring

Other: ____________

Upload the policy/guidance:

or URL____________

Indicate where in the evidence the relevant information can be found____

No

LPO1

3 points , G

Guidance document(s) used for commercial real estate lending that include sustainability aspects. Participants must upload document evidence, and select applicable use case(s).

Select Yes or No. If Yes, please select all applicable checkboxes and a radio button.

Radio buttons: Only one answer is possible. Please select the most applicable.

Other: Answers provided under 'Other' must be outside the options listed in the indicator to be valid. State a loan origination and/or follow-up step when this guidance document is used/applied.

Reporting period: Answer must refer to the reporting period as identified in EC5.

Reporting level: Answer provided must refer to the entity / business unit, not a broader organization.

For real estate debt funds and MREITs this means that response should be provided at the fund / entity level.

For institutional lenders and others this refers to the real estate lending [unit] within the organization.

The evidence and ‘other’ answer provided will be subject to manual validation.

Document upload or hyperlink: The evidence should sufficiently support all the items selected for this question. If a hyperlink is provided, ensure that it is active and that the relevant page can be accessed within two steps. It is possible to upload multiple documents, as long as it’s clear where information can be found. A piece of supporting evidence document or URL cannot be uploaded for more than one disclosure method selected, i.e., identical documents will not be accepted for more than one disclosure type.

Evidence may include but are not limited to:

See Appendix 3 - Validation for additional information about GRESB Validation.

3 points, G

Scoring of this indicator is equal to the fraction assigned to the selected option, multiplied by the total score of the indicator.

Evidence: The evidence is manually validated and points are contingent on the validation decision.

Other: The 'Other' answer is manually validated and points are contingent on the validation decision.

See the Scoring Document for additional information on scoring.

Collateral assessment: Process that evaluates property pledged by a borrower to secure a loan.

Loan approval: Formal authorization from lender that allows borrower to receive a loan.

Loan monitoring: Systematic approach on gathering of loan specific KPIs throughout the loan term.

Loan screening: Internal process focused on gathering and analysing available data related to the loan. It also includes uncovering and acknowledging risks associated with a specific lending decision.

LPO2

Does the document referenced in LPO1 include specific sustainability-related requirements?

Yes

Select included metrics/aspects:

Asset-specific metrics

Green Building Certification

Energy Rating

Historical performance

Energy consumption

Water consumption

Waste diversion

Other: ____________

Other: ____________

Project scope

New construction

Major renovation/deep retrofit

Refurbishment

Other: ____________

Property types applicable

Retail

Office

Industrial

Residential

Hotel

Lodging, Leisure & Recreation

Education

Technology/Science

Healthcare

Mixed Use

Other: ____________

Regional/location considerations

Other: ____________

Provide context on the practical use of this guidance, its implementation, and connection to achieving the Lender's sustainability objectives

________________________

No

Not Applicable

LPO2

3 points , G

Participants should select all sustainability-related requirements that are present in the commercial real estate lending policy/guidance document (see LPO1). Please elaborate on implementation actions.

Select Yes or No. If Yes, please select applicable checkboxes and complete the open text box.

This indicator contains four options to provide an answer. After selecting Yes, state the sustainability-related metrics included in the guidance document.

Open text box: Description provided should fully support each checkbox selected, along with the following elements:

Other: Answers provided under 'Other' must be outside the options listed in the indicator to be valid.

Other: State the specific sustainability-related metric/aspect which is included in the guidance document. Ensure that the other answers provided are not a duplicate of a selected option above. The 'Other' answers are manually validated.

See Appendix 3 - Validation for additional information about GRESB Validation.

3 points, G

Scoring is based on the number of selected options. It is not necessary to select all options to achieve the maximum score.

Other: The 'Other' answer is manually validated and points are contingent on the validation decision.

Open text box: The open text box is not scored and is for reporting purposes only.

See the Scoring Document for additional information on scoring.

Energy consumption: the use of energy by the asset.

Energy Rating: A scheme that measures the energy efficiency performance of buildings.

Green building certificate: Recognition that a project has received a green building rating. A certificate indicates the name and location of the project, version of the rating system, date of certification, and level of recognition.

Industrial: Includes distribution warehouses, flex, manufacturing and self-storage.

Major Renovations: Alterations that affect more than 50 percent of the total building floor area or cause relocation of more than 50 percent of regular building occupants. Major renovation projects refer to buildings that were under construction at any time during the reporting year.

New construction: Includes all borrower activities to obtain or change building or land use permissions and financing.

Office: Includes free-standing office, office terrace, unattributed office buildings, office parks, and medical offices.

Refurbishment: Renovation or redecoration works undertaken by a landlord or tenant.

Residential: Refers to buildings with at least five residential units including apartments and student housing.

Waste diversion: Actions that focus on diverting wastes from landfills. This may include actions to decrease waste reduction at the source and recycling and reusing materials that are non-biodegradable.

Water consumption: the use of water resources by the asset.

Management: Reporting

Management: ReportingInstitutional investors and other shareholders are primary drivers for greater sustainability reporting and disclosure among entities. Real estate lenders share how ESG management practices and performance impacts the business through formal internal / external disclosure mechanisms.

This aspect evaluates how the entity communicates its ESG actions and/or performance.

LRP1

ESG reporting

Does the lender disclose its ESG actions and/or performance?

Yes

Please select all applicable options (multiple answers possible)

Section in Annual Report

Select the applicable reporting level

Investable Entity / Real Estate Loan Portfolio

Investment manager

Group

Aligned with Guideline name

Disclosure is third-party reviewed:

Yes

Externally checked

Externally verified

using Scheme name

Externally assured

using Scheme name

No

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

Stand-alone sustainability report(s)

Select the applicable reporting level

Investable Entity / Real Estate Loan Portfolio

Investment manager

Group

Aligned with Guideline name

Disclosure is third-party reviewed:

Yes

Externally checked

Externally verified

using Scheme name

Externally assured

using Scheme name

No

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

Integrated Report

*Integrated Report must be aligned with IIRC framework

Select the applicable reporting level

Investable Entity / Real Estate Loan Portfolio

Investment manager

Group

Disclosure is third-party reviewed:

Yes

Externally checked

Externally verified

using Scheme name

Externally assured

using Scheme name

No

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

Dedicated section on corporate website

Select the applicable reporting level

Investable Entity / Real Estate Loan Portfolio

Investment manager

Group

URL____________

Indicate where in the evidence the relevant information can be found____

Other: ____________

Select the applicable reporting level

Investable Entity / Real Estate Loan Portfolio

Investment manager

Group

Aligned with Guideline name

Disclosure is third-party reviewed:

Yes

Externally checked

Externally verified

using Scheme name

Externally assured

using Scheme name

No

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

No

RP1

4 points , G

This indicator assesses the level of ESG disclosure undertaken by the entity. It also evaluates the entity’s use of third-party ESG reporting review to ensure the reliability, integrity, and accuracy of ESG disclosure. Disclosure of ESG information and performance demonstrates an entity’s transparency in explaining how ESG policies and management practices are implemented by the entity, and how these practices impact the business. In addition, third-party ESG disclosure review increases investors’ confidence in the information disclosed.

Select yes or no. If yes, select all applicable sub-options.

In all cases:

The full list of accepted schemes is found in Appendix 8 - Assurance and Verification Schemes of the Reference Guide. Additional schemes may also receive recognition if they meet GRESB’s criteria. To submit a new scheme for review, please contact the GRESB team. The final deadline for submitting a new assurance/verification scheme for review by the GRESB team is March 15th. Schemes submitted for review after March 15th will not be reviewed until the subsequent reporting year.

The evidence and ‘other’ answer provided will be subject to manual validation.

Other: Add a disclosure method that applies to the entity but is not already listed. Ensure that the ‘Other’ answer provided is not a duplicate or subset of another option selected. It is possible to report multiple ‘Other’ answers. If multiple ‘Other’ answers are acceptable, only one will be counted towards scoring.

Document upload or hyperlink: The evidence should sufficiently support all the items selected for this question. If a hyperlink is provided, ensure that it is active and that the relevant page can be accessed within two steps. It is possible to upload multiple documents, as long as it’s clear where information can be found. A piece of supporting evidence document or URL cannot be uploaded for more than one disclosure method selected, i.e., identical documents will not be accepted for more than one disclosure type.

General evidence requirements:

Specific evidence requirements per disclosure type:

Evidence requirements IR report: The document upload or URL provided must contain clear evidence of alignment with the IFRS Integrated Reporting Framework (formerly the International Integrated Reporting Council (IIRC) Integrated Reporting Framework (December 2013)) within the report itself. Note that references to the IFRS accounting standards, IFRS S1 or S2, and SASB are not equivalent. Integrated reports can reference 2024, 2023, or 2022 performance and/or actions.

Evidence requirements Annual Report: Annual Reports should cover the reporting year as described in EC4. Annual Reports from the prior reporting year detailing actions and/or performance are acceptable if it is explicitly stated that the Annual Report for the current reporting year has not yet been published. If an entity reports on a semi-annual basis, both semi-annual reports must be uploaded to cover the 12 months of reporting identified in EC4. Similarly, if an entity reports quarterly, all 4 quarterly reports must be uploaded to cover the 12 months of reporting identified in EC4.

Evidence requirements Standalone sustainability report: Sustainability reports referencing the current or previous reporting year as described in EC4 are accepted.

Evidence requirements Dedicated section on corporate website: The webpage(s) must include ESG actions and/or performance undertaken by the entity during the reporting year as given in EC4, explicitly addressing at least one pillar of ESG (but can address all three ESG pillars). A hyperlink to the Annual Report or Sustainability Report, or any other documents are not valid. In addition, a list of general goals and/or commitments on the website is not sufficient.

Evidence requirements ‘Other’: An additional disclosure method such as third-party forms of disclosure like CDP Questionnaires or UN PRI Transparency Reports is considered valid. Disclosure methods with a different reporting level can also be provided (i.e. if an entity-level ESG report is provided for Stand-alone sustainability report, a group-level ESG report can be provided for ‘Other’.) Quarterly updates, Board reports, investor presentations, newsletters, or press releases disclosing ESG actions and/or performance are considered valid. Ensure applicability to the reporting year as provided in EC4 based on the actions and/or performance disclosed.

See Appendix 3 - Validation for additional information about GRESB Validation.

4 points, G

Scoring is based on the number of selected options. It is not necessary to select all options to achieve the maximum score.

Evidence: The evidence is manually validated and points are contingent on the validation decision.

Other: The 'Other' answer is manually validated and points are contingent on the validation decision.

See the Scoring Document for additional information on scoring.

Alignment: To agree and match with a recognized sustainability standard (either voluntary or mandatory).

Annual report: A yearly record of an entity’s financial performance that is distributed to investors under applicable financial reporting regulations.

Externally checked: Applies to instances when a third party has reviewed the data in a structured and consistent process, but no official certification has been awarded.

Externally verified: Applies to instances where a third party has reviewed the reporting against an existing scheme. When this checkbox is ticked, participants must select the scheme name from the dropdown.

Externally assured: Applies to instances where a third party has reviewed the data against an existing scheme. When this checkbox is ticked, participants should select the scheme name from the dropdown.

Note: GRESB treats verification and assurance equally in the context of the assessment.

Dedicated section on corporate website: A section of the entity’s website that explicitly addresses ESG performance.

Disclosure: The act of making information or data readily accessible and available to all interested individuals and institutions. Disclosure must be external and cannot be an internal and/or ad hoc communication within the participating entity.

ESG actions: Specific activities performed to improve management of environmental, social and governance issues within the entity.

ESG performance: Reporting of material indicators that reflect implementation of environmental, social, or governance (ESG) management.

Group: Select this reporting level if the report (e.g., Annual Report) includes the entity being assessed but presents data aggregated for the broader group of companies to which the entity belongs, without detailed performance data specific to the entity itself.

Integrated Report: A report that is aligned with the requirements of the International Financial Reporting Standards Foundation (IFRS) Integrated Reporting Framework (formerly the International Integrated Reporting Council (IIRC) Integrated Reporting Framework). Integrated reporting joins relevant information about both the entity's financial and non-financial strategy, governance, performance, and prospects in a manner that conveys the holistic commercial, social, and environmental context in which it operates.

Investable Entity / Real Estate Loan Portfolio: Select this reporting level if the disclosure (e.g., Annual Report) directly references the investable entity / Real Estate Loan Portfolio being assessed. This includes disclosures that provide specific and detailed actions or performance data for the book submitted in the GRESB Assessment, even if the report also covers other investable entities / Real Estate Loan Portfolios. In case you are a real estate lending unit of a bank or an insurance company, you are submitting the Assessment for the Real Estate Loan Portfolio of your financial organization and the disclosure specifically mentions the Real Estate Loan side of the organization, this option should be selected.

Investment Manager: Select this reporting level if the disclosure (e.g., Annual Report) includes the entity being assessed but does not provide specific or detailed performance data for it. Instead, the disclosure focuses on aggregated information about the investment management entity or company overseeing the participating entity.

Standalone sustainability report: A report solely dedicated to sustainability or ESG performance.

Reporting Level:

ANREV Sustainability Reporting Guidelines, 2016

EPRA Best Practices Recommendations on Sustainability Reporting, 3rd version, September 2017

GRI Sustainability Reporting Guidelines, 2016: 202-1; 205-3; 308-2

308-2 IIRC Integrated Reporting Framework, 2013

INREV Sustainability Reporting Guidelines, 2023

Management: Risk Management

Management: Risk ManagementThis aspect evaluates the processes used by the entity to support ESG implementation and investigates the steps undertaken to recognize and prevent material ESG related risks.

LRM1

Process to implement governance policies

Does the lender have processes to implement governance policy/policies?

Yes

Select all applicable options (multiple answers possible)

Compliance linked to employee remuneration

Dedicated help desks, focal points, ombudsman, hotlines

Disciplinary actions in case of breach, i.e. warning, dismissal, zero tolerance policy

Employee performance appraisal systems integrate compliance with codes of conduct

Responsibilities, accountabilities and reporting lines are systematically defined in all divisions and group companies

Training related to governance risks for employees (multiple answers possible)

Regular follow-ups

When an employee joins the organization

Whistle-blower mechanism

Other: ____________

No

Not applicable

RM2

2 points , G

This indicator examines specific actions taken to limit exposure to governance-related risks. It refers to the implementation of the policy that addresses risks from exposure to governance issues.

Select yes or no. If yes, select all applicable sub-options.

Other: State the other system or procedure in place. Ensure that the other answer provided is not a duplicate of a selected option above (e.g., Anti-bribery training when 'Training related to governance risks for employees' is selected). It is possible to report multiple other answers. If multiple other answers are acceptable, only one will be counted towards scoring

See Appendix 3 - Validation for additional information about GRESB Validation.

2 points, G

Scoring is based on the number of selected options. It is not necessary to select all options to achieve the maximum score.

Other: The 'Other' answer is manually validated and points are contingent on the validation decision.

See the Scoring Document for additional information on scoring.

Governance risks for employees: Examples can include, but are not limited to: bribery and corruption risks, insider trading, sharing of confidential information.

Regular follow-ups: Training offered at least once a year to employees, starting from their second year of employment.

Training related to governance risks for employees: Employee training ensures that employees understand and adhere to the laws, regulations and internal corporate policies that apply to their daily roles is essential to ensuring that compliance regulations are met in the workplace.

Whistle-blower mechanism: A process that offers protection for individuals that want to reveal illegal, unethical or dangerous practices. An efficient whistle-blower mechanism prescribes clear procedures and channels to facilitate the reporting of wrongdoing and corruption, defines the protected disclosures, outlines the remedies and sanctions for retaliation.

OECD Cleangovbiz, “Whistleblower protection: encouraging reporting”, 2012

LRM2

ESG due diligence for new loan originations

Does the lender perform asset-level environmental and/or social risk assessments as a standard part of its due diligence process for new loan originations?

Yes

Select all issues included (multiple answers possible)

Biodiversity and habitat

Building safety

Climate/Climate change adaptation

Compliance with regulatory requirements

Contaminated land

Energy efficiency

Energy supply

Flooding

GHG emissions

Health and well-being

Indoor environmental quality

Natural hazards

Socio-economic

Transportation

Waste management

Water efficiency

Water supply

Other: ____________

No

Not applicable

RM4

4 points , G

This indicator identifies if the entity performs asset-level environmental and/or social assessments as a standard part of the due diligence process for new originations.

Risk assessments help to reduce exposure to long-term sustainability risks. Integration of sustainability risk assessments into the origination process demonstrates a commitment to ESG management, a focus on mitigating risks that might impact returns, and a forward-looking approach to the development of the portfolio.

Select yes or no. If yes, select all applicable sub-options.

Other: State the other risk factor assessed. Ensure that the other answer provided is not a duplicate of a selected option above (e.g., seismic assessments when ‘Natural hazards’ is selected). It is possible to report multiple other answers. If multiple other answers are acceptable, only one will be counted towards scoring.

See Appendix 3 - Validation for additional information about GRESB Validation.

4 points, G

Scoring is based on the number of selected options. It is not necessary to select all options to achieve the maximum score.

Other: The 'Other' answer is manually validated and points are contingent on the validation decision.

See the Scoring Document for additional information on scoring.

Biodiversity and habitat: Issues related to wildlife, endangered species, ecosystem services, habitat management, and relevant topics. Biodiversity refers to the variety of all plant and animal species. Habitat refers to the natural environment in which these plant and animal species live and function.

Building safety: Environmental issues with the potential to create or exacerbate risks to human safety. Examples of building safety topics include fire safety, structural safety, and electrical and gas safety during development. Building safety strategies can include, but are not limited to, having site inspections at key construction milestones, having a reporting system in place for recording building safety observations, and having designated personnel to oversee building safety compliance during development.

Climate change adaptation: Preparation for long-term change in climatic conditions or climate related events. Examples of climate change adaptation measures can include, but are not limited to: building flood defenses, xeriscaping and using tree species resistant to storms and fires, adapting building codes to extreme weather events.

Compliance with regulatory requirements: Examples include, but are not limited to: mandatory energy/carbon disclosure schemes, changes in taxes e.g. carbon tax, extreme volatility in energy prices due to regulation, zoning.

Contaminated land: Land pollution which may require action to reduce risk to people or the environment. As an example, contamination can be assessed through a Phase I or II Environmental Site Assessment.

Due diligence process: The process through which a potential lender evaluates a target asset for an origination, contributing to well-informed investment decision-making.

Energy efficiency: Refers to products or systems using less energy to provide the same consumer benefit.

Energy supply: Availability of conventional power (generated by the combustion of fuels: coal, natural gas, oil) or renewable energy (e.g. sun, wind, water, organic plant and waste material).

Environmental risks: Impact on living and non-living natural systems, including land, air, water and ecosystems. This includes, but is not limited to biodiversity, transport and product and service-related impacts, as well as environmental compliance and expenditures.

Greenhouse gas emissions: GHGs refers to the seven gases listed in the GHG Protocol Corporate Standard: carbon dioxide (CO2); methane (CH4); nitrous oxide (N2O); hydrofluorocarbons (HFCs); perfluorocarbons (PFCs); nitrogen trifluoride (NF3) and sulfur hexafluoride (SF6). They are expressed in CO2 equivalents (CO2e).

Employee health & well-being: The health & well-being of employees responsible for the entity.

Indoor environmental quality: Refers to the conditions inside the building. It includes air quality, access to daylight and views, pleasant acoustic conditions and occupant control over lighting and thermal comfort.

Natural hazards: Naturally occuring physical phenomena that have the potential to cause serious disruptions to the functioning of a community. Natural hazards can be geophysical, hydrological, climatological, meteorological, or biological. Examples include but are not limited to earthquakes, wildfires, hurricanes, and droughts.

Risk assessment: Careful examination of the factors that could potentially adversely impact the value or longevity of a real estate asset. The results of the assessment assist in identifying measures that have to be implemented in order to prevent and mitigate the risks.

Socio-economic risks: Impact on social well-being, livelihoods and prosperity of local communities and individuals. Examples include: economic/political instability, social housing, vulnerability to pandemics and epidemics, crime and vandalism, and the displacement of people.

Transportation risks: Risks associated with transportation around the location of a building in relation to pedestrian, bicycle and mass-transit networks, in context of the existing infrastructure and amenities in the surrounding area.

Waste management: Issues associated with hazardous and non-hazardous waste generation, reuse, recycling, composting, recovery, incineration, landfill and on-site storage.

Water efficiency: Refers to the conservative use of water resources through water-saving technologies to reduce consumption.

Water supply: Provision of surface water, groundwater, rainwater collected directly or stored by the entity, waste water from another organization, municipal water supplies or other water utilities, usually via a system of pumps and pipes.

World Economic Forum, Global Risks, 2014 Environment Agency, Groundwater protection: Principles and practice, 2013

World Health Organization

SASB-Real Estate Owners, Developers & Investment Trusts (March 2016): IF0402-05; IF0402-09; IF0402-14