Reporting entity

Entity name: ____________

Fund Manager Organization Name (if applicable): ____________

The 2024 GRESB Real Estate Assessment Document accompanies the 2024 GRESB Real Estate Assessment and is published both as a standalone document and in the GRESB Portal alongside each Assessment indicator. The Assessment Document reflects the opinions of GRESB and not of our members. The information in the Assessment Document has been provided in good faith and on an “as is” basis. We take reasonable care to check the accuracy and completeness of the Assessment Document prior to its publication. While we do not anticipate major changes, we reserve the right to make modifications to the Assessment Document. We will publicly announce any such modifications.

The Assessment Document is not provided as the basis for any professional advice or for transactional use. GRESB and its advisors, consultants and sub-contractors shall not be responsible or liable for any advice given to third parties, any investment decisions or trading or any other actions taken by you or by third parties based on information contained in the Assessment Document.

Except where stated otherwise, GRESB is the exclusive owner of all intellectual property rights in all the information contained in the Assessment Document.

Mission-driven and investor-led, GRESB is the environmental, social and governance (ESG) benchmark for real assets. We work in collaboration with the industry to provide standardized and validated ESG data to the capital markets. The 2023 real estate benchmark covers more than 2,000 property companies, real estate investment trusts (REITs), funds, and developers. Our coverage for infrastructure includes over 850 infrastructure funds and assets. Combined, GRESB represents USD 8.8 trillion in real asset value. More than 150 institutional investors, with over USD 50 trillion AUM, use GRESB data to monitor their investments, engage with their managers, and make decisions that lead to a more sustainable real asset industry.

For more information, visit gresb.com and follow GRESB on LinkedIn.

The GRESB Real Estate Assessment is the global standard for ESG benchmarking and reporting for listed property companies, private property funds, developers and investors that invest directly in real estate. The Assessment evaluates performance against three ESG Components - Management, Performance, and Development. The methodology is consistent across different regions, investment vehicles and property types and aligns with international reporting frameworks, such as TCFD, GRI and PRI.

The GRESB Real Estate Assessment provides investors with actionable information and tools to monitor and manage the ESG risks and opportunities of their investments, and to prepare for increasingly rigorous ESG obligations. Assessment participants receive comparative business intelligence on where they stand against their peers, a roadmap with the actions they can take to improve their ESG performance and a communication platform to engage with investors.

GRESB works in close collaboration with the National Association of Real Estate Investments Trusts (Nareit), a GRESB Industry Partner and Nareit encourages its members to complete the annual GRESB Real Estate Assessments to demonstrate their sustainability leadership. Since 2012, Nareit has awarded REITs across several property sectors a Leader in the Light Award based on their Real Estate Assessments, as well as a supplemental submission evaluating their organizational strategies and performance.

The GRESB Real Estate Assessments will continue to be the basis for their annual Leader in the Light Award competition, however this year, the supplemental submission will be completed separately from the GRESB Assessment. To participate in the Leader in the Light Award program, Nareit members must complete both the GRESB Real Estate Assessment and the separate supplement, administered by Nareit. Once all sections of the GRESB Real Estate Assessment are completed and the supplement submitted to Nareit, participants will automatically be included in the Leader in the Light Award competition. Leader in the Light Awards will be presented to the winners in November.

Participants should contact Nareit directly in case they have any questions.

GRESB Public Disclosure evaluates the level of ESG disclosure by listed property companies and investment vehicles for an entire investable universe. The evaluation is based on a set of indicators aligned with the GRESB Real Estate and Infrastructure Assessments. It provides investors with a resource hub to access ESG disclosure documents across their full listed investment portfolio and make comparisons against an investable universe with full coverage.

GRESB Public Disclosure data is initially collected by the GRESB team for selected companies, including both 2023 GRESB Real Estate and Infrastructure Asset Assessment participants and non‑participants. All data collected must come from publicly available sources, private documents are not accepted.

All constituents have the opportunity to review and update the data collected prior to it becoming accessible to GRESB Listed Investor Members. GRESB Public Disclosure consists of four Aspects: Governance of Sustainability, Implementation, Operational Performance and Stakeholder Engagement. Together, these Aspects contribute towards a Public Disclosure Level, expressed through an A to E sliding scale.

The Real Estate Assessment generates two benchmarks: The GRESB Real Estate Standing Investments Benchmark and the GRESB Development Benchmark.

The Real Estate Standing Investments Benchmark consists of participants completing both the Management and Performance Components and the Development Benchmark consists of participants completing both the Management and Development Components.

GRESB does not require participation in any of the Assessment Components. However, if the entity does have both standing investments and development projects and considers itself both an operator of buildings and involved in development activities, it is highly recommended to participate in both benchmarks. As a result, participants will receive two GRESB Scores, two Benchmark Reports, two peer groups, etc. capturing how the entities approach their respective activities in both benchmarks.

GRESB’s global benchmark uses a consistent methodology to compare performance across different regions, investment vehicles, and property types. This consistency, combined with our broad market coverage, means our members and participants can apply a single, globally recognized ESG framework to all their real estate investments.

GRESB results provide a practical way to understand ESG performance and communicate it to investors and other stakeholders. GRESB provides overall scores of ESG performance - such as the GRESB Score and GRESB Ratings - as well as detailed aspect-level and individual indicator-level assessments of performance. The key to analyzing GRESB data is in peer group comparisons that take into account country, regional, sectoral and investment type variations. This richer analysis enables fund managers and companies to understand their results in the context of their investment strategies and communicate this to their investors.

GRESB is committed to facilitating the use of its ESG metrics in investment decision-making processes and encouraging an active dialogue between investors, fund managers and companies on ESG issues. GRESB updates its Investor Member Guidance on an annual basis to assist GRESB Investor Members in their engagement with managers.

The Assessment Portal opens on April 1, 2024. The submission deadline is July 1, 2024 (23:59:59 PST), providing participants with a three‑month window to complete the Assessment. This is a fixed deadline, and GRESB will not accept submissions received after this date. GRESB validates and analyzes all participants’ Assessment submissions.

The GRESB validation process starts on June 15, 2024 and continues until July 31, 2024. Participants may be contacted during this time to clarify any issues with their response.

In 2020 GRESB introduced a new Review Period in the Assessment Cycle to further strengthen the reliability of the Assessments and benchmark results. The Review Period will start on September 2, when preliminary individual GRESB results will be made available to all participants and run for the month. During the Review Period, participants will be able to submit an Assessment Correction Request to GRESB.

The final results will be launched to both Participant and Investor Members on October 1. Public Results events and other results outputs will be scheduled in October and November.

For more information about the 2024 Assessment timeline, click here.

A Pre-submission Check is a high-level check of a participant’s submission. The Pre-Submission Check is carried out by GRESB’s third party validation provider Sustainability Assurance Services (SAS) and features a careful review of your Assessment response followed by a 1-hour discussion call. After the discussion call, you will receive a feedback report highlighting issues found. You can also choose to only receive a feedback report, without a call. You can request a Pre-Submission Check for all reporting entities and we encourage all participants to do so.

The Pre-Submission Check does not exclude the participant from any element of the validation process, nor does it guarantee a higher GRESB Score. It is intended to ensure that no important details have been overlooked in the submission and provides the opportunity to ask for additional guidance and clarification on the GRESB Assessment indicators. The Pre-Submission Check helps reduce errors that may adversely impact Assessment results and identifies inconsistent responses and incorrect answer formats.

The Pre-Submission Check is available for request from April 1 to June 1, 2024 (11:59:59 p.m., PST) subject to available time slots. We strongly encourage participants to place their requests as early as possible. The Pre-Submission Check can be requested before the Assessment has been completed, but the scope of the review will be limited to the information filled in one week prior to the call.

The Assessment Portal includes indicator-specific guidance, available under the “Guidance” tab that explains:

In addition to the guidance in the Portal, each Assessment is accompanied by a Reference Guide. The Reference Guide provides introductory information on the Assessments and a report-format version of the indicator-by-indicator guidance that is available under the Guidance tab in the Portal.

GRESB works with a select group of Partners who can help participants with their Assessment submission. To learn more about the services offered by GRESB Partners, take a look at our Partner Directory.

Participants are able to contact the GRESB Helpdesk at any time for support and guidance.

GRESB Real Estate Assessment Training is designed to help participants, potential participants and other GRESB stakeholders (managers, consultants, data partners) improve their ESG reporting through the GRESB Real Estate Assessment.

GRESB provides a free online training platform in 2024. The training courses are modular and self-paced, walking participants through the various aspects of the Assessments, and providing detailed examples and tips for a successful submission.

Data is submitted to GRESB through a secure online platform and can only be seen by current GRESB Staff or authorized personnel from GRESB’s third-party validation provider SAS. GRESB benchmark scores are not made public. For listed entities, the entity name is disclosed on the GRESB website. For non-listed entities, the fund manager’s name is disclosed.

Access to Assessment results

Data collected through the GRESB Real Estate Assessment is only disclosed to the participants themselves and:

No other third parties will see the data. GRESB Investor Members must request access to a participant’s Benchmark results and scores, allowing the participant the control to either accept or deny this request.

Access to uploaded evidence

Documentation provided as evidence can be made available to GRESB Real Estate Investor Members on a document by document basis. Each uploaded document has a checkbox (with the default set to ‘not available’) which, when selected by the participant, makes this evidence available to all investors with access to that entity. It is not possible to choose a subset of investors which you would like to share the documents with.

Access to peer group results:

GRESB provides an opt-in option that will disclose the entity’s name (public) or fund manager’s name (private), as well as the scores for the different Components, to participants in the GRESB Universe that also opted to disclose their name and Component scores.

As a default, GRESB does not disclose a participant’s data to other participants. For listed entities, the entity name is disclosed in the Benchmark Report, as well as the entity names of listed peer group constituents. For non-listed entities, only the fund manager’s name is disclosed, as well as the fund manager’s name of private peer group constituents.

Access to asset-level data:

The 2024 Assessment requires participants to report the indicators on Energy, GHG, Water, Waste, Building Certifications, and Efficiency Measures at the asset level. This asset-level data provided to GRESB is strictly confidential and will only be used to check and validate the aggregated portfolio performance data. It will not be passed on to any external party, be it investors or others, in any way that allows the data to be traced back to the asset, without the explicit consent of the participant.

GRESB has developed a number of tools to assist participants with the collection and aggregation of asset-level data that is required to complete certain aspects of the Assessment. Property companies and funds are encouraged to use the asset level tools to streamline data flows, and to increase data quality. The asset-level data provided to GRESB is strictly confidential and will only be used for aggregation to portfolio level. No individual asset level information will be disclosed to participants’ investors.

Asset-level data will be used in an aggregated form, and non-traceable manner, in the following ways:

The main driver for asset level reporting is to improve investor confidence in data quality. In addition, it enables us to provide participants with additional insights into the impact of their ESG programs, the basis for and paves the way for more tailored assessments in the future.

GDPR compliance:

GRESB is fully compliant with GDPR. The GRESB Privacy Statement can be found here. We also have specific internal policies, such as our Data Breach Policy and our Data Protection Policy, related to GDPR that we cannot share externally for security reasons. Please note that asset level data does not fall under the incidence of GDPR because it does not contain any personal data.

Cybersecurity:

GRESB’s data security measures and systems have been reviewed by an external expert and no issues were flagged. The GRESB website and the GRESB Portal are fully HTTPS/TLS encrypted. GRESB has strict and extensive policies on data security that cannot be shared externally for security reasons.

First year participants can submit the Assessment without providing GRESB Investor Members with the ability to request access to their results. This is referred to as a “Grace Period”.

First year participants wishing to report under the Grace Period can select the option on an entity-by-entity basis from the settings section in the Assessment Portal. Participants who select the “Grace Period” option can decide to unselect the option following receipt of their results. The Grace Period is not available in the second year of participation, regardless of whether it was used in the first year or not.

The “Grace Period” allows participants a year to familiarize themselves with the GRESB reporting and assessment process. The names of participating entities are still visible during the Grace Period, but GRESB Investor Members will not be able to request to see their results.

The GRESB Assessment Portal has the following tools and functionality to help ensure an efficient and accurate submission:

The tools are designed to streamline data flows and increase data quality.

In 2024, participants can use the online GRESB Asset Portal or a data partner system to upload asset-level data for the following indicators:

Each indicator is allocated to one of the three ESG dimensions (E- environmental; S- social; G- governance):

The score breakdown by the E, S, G dimensions within each component is presented below.

| E | S | G | |

|---|---|---|---|

| Management | 0% | 35% | 65% |

| Performance | 89% | 11% | 0% |

| Development | 73% | 21% | 6% |

Every indicator in the 2024 Assessment can be answered with ‘Yes’ or ‘No’ and in some cases with ‘Not applicable’. If ‘Yes’ is selected, the participant has the option to further classify the response by selecting one or more sub-options.

Participants should select all sub-options that accurately describe the entity and for which the entity can provide evidence. If ‘No’ or ‘Not applicable’ is selected, the participant may not select any additional sub-options. “A Not Applicable” answer is interpreted and scored in the same way as a “No” and will yield 0 points.

Selected indicators in the Assessment require supporting evidence. Evidence is information that can be used to validate the overall answer to the indicator and support the additionally selected criteria.

GRESB does not have a prescriptive standard for evidence, rather the expectation is that a validator with reasonable domain expertise can review the evidence and find support for the overall indicator response and selected answer options. This means that the uploaded evidence must clearly reference the answer options selected by the participant. The evidence must not require extensive interpretation or inference, and participants are strongly encouraged to provide the simplest evidence that supports their claim.

If a hyperlink (or deep link) is provided, ensure that the relevant page can be accessed within two steps. Ideally, the landing page should contain all the information needed to validate the answer. To qualify as valid supporting evidence, the evidence provided must demonstrate the existence of the relevant topic relating to each of the criteria selected. The participant has the obligation to ensure that the hyperlink is functioning. Broken links are the responsibility of the participant and will be interpreted as the absence of evidence. Hyperlinks can only be provided if indicated. In all other instances, the actual document should be uploaded. Hyperlinks in uploaded documents will not be checked.

All Assessment responses must be submitted in English.

Providing Evidence in Other Languages

Documents uploaded as supporting evidence do not need to be entirely translated. However, for evidence provided in languages other than English, a thorough summary sufficient to convey the requirements have been met is required for validation purposes. Participants may make use of the open text box to provide the document(s) summary. In addition, each selected issue must be identified in the evidence uploads by providing page number and exact location such as paragraph, clause, sentence, bullet number, etc.

Translation of the GRESB Assessment

The GRESB Assessment Portal can be translated by using “Google translate” via the Google Chrome web browser. This applies to the Assessment Portal, guidance notes, and online version of the Reference Guide.

How to use Google Translate:

Turn translation on

You can control whether Chrome will offer to translate web pages.

Disclaimer

Please note that not all text may be translated accurately or be translated at all. GRESB is not responsible for incorrect or inaccurate translations. GRESB will not be held responsible for any damage or issues that may result from using Google Translate.

Over the years, the number of scored open text boxes has been reduced to zero in an effort to shift focus from management to performance. Open text boxes are now only used for reporting purposes and to provide additional context for a subset of indicators. Note that the contents of the open text boxes are included in the GRESB Benchmark Report.

Many indicators offer the opportunity to provide an alternative answer option (‘Other’). These other answers must be distinct from the options listed in the question. It is possible to add multiple other answers, however scores will not be aggregated. All Other answers are validated as part of the data validation process.

The indicator-specific guidance contains:

Answers must refer to the reporting year identified in EC4: Reporting year in the Real Estate Assessment, unless the indicator specifies otherwise.

A response to an indicator must be true at the close of the reporting year; however, the response does not need to have been true for the entire reporting year. For example, if a policy was put in place one month prior to the end of the reporting year, this is acceptable, it need not have been in place for the entire reporting year. GRESB does not favour the use of calendar year over fiscal year or vice versa, as long as the chosen reporting year is used consistently throughout the Assessment.

Answers must be applicable to the entity level. When a participating entity is part of a larger investment management organization or group of companies (the ‘Organization’), GRESB participants should use the open text box to explain how the answers apply to the entity.

In the GRESB Terms and Conditions, the term ‘Participating Portfolio’ refers to a ‘(Reporting) Entity’ as used in the in the GRESB Assessments, Guidance materials (e.g., Reference Guides and Scoring documents), GRESB Products (e.g., Benchmark Reports and PAT), the GRESB Portal, and in GRESB Training materials.

The Real Estate Assessment is structured in three components: Management, Performance and Development:

Each Component is divided into Aspects; aspects comprise of individually scored indicators. This Reference Guide provides detailed insight into the points available for each indicator, and the weighting of Assessment aspects. The information in this section provides additional context. Points per indicator are determined by the GRESB Foundation in advance of the Assessment opening for responses. Indicator scoring goes through a three-stage review process based on GRESB’s rules, principles and guidelines.

Points Per Indicator

For indicators where you can select one or more answers, GRESB awards points cumulatively for each individual selected answer and then aggregates to calculate a final score for the indicator. For many indicators, this final score is capped at a maximum, meaning it is not necessary to select all answers to receive full points. This scoring mechanism allows the diversity among property companies and funds and the variety of their sustainability-oriented activities to be reflected. Supporting evidence and open fields for which participants select ‘other’ answers, are manually validated. Points are awarded based on the validity of the response.

Scoring Model

The scoring model is based on an automated system, which uses a technology platform designed for GRESB by a third party that specializes in data analysis software development. The scoring is completed without manual intervention after data validation has been completed.

The sum of the scores for each indicator adds up to a maximum of 100 points. The maximum score for each aspect is a weighted element of the overall GRESB Score. GRESB takes into account the unique characteristics of different property types, not only in benchmarking absolute scores, but also in the scoring of a selection of indicators. A selection of indicators is scored based on each portfolio’s main property types – this holds specifically for the Energy, GHG, Water, Waste and Building Certifications indicators.

The max Overall Score = 100, corresponding to 100 points, can be obtained as follows:

| Component | Aspect | # Points | % Component | % Overall Score |

|---|---|---|---|---|

| Management | Leadership | 7 | 23% | 7% |

| Policies | 4.5 | 15% | 5% | |

| Reporting | 3.75 | 13% | 4% | |

| Risk Management | 4.75 | 16% | 5% | |

| Stakeholder Engagement | 10 | 33% | 10% | |

| Total | 30 | 100% | 30% | |

| Performance | Risk Assessment | 9 | 13% | 9% |

| Targets | 2 | 3% | 2% | |

| Tenants & Community | 11 | 16% | 11% | |

| Energy | 14 | 20% | 14% | |

| GHG | 7 | 10% | 7% | |

| Water | 7 | 9.5% | 7% | |

| Waste | 4 | 5.5% | 4% | |

| Data Monitoring & Review | 5.5 | 8% | 6% | |

| Building Certifications | 10.5 | 15% | 11% | |

| Total | 70 | 100% | 70% | |

| Development | ESG Requirements | 12 | 17% | 12% |

| Materials | 6 | 9% | 6% | |

| Building Certifications | 13 | 19% | 13% | |

| Energy | 14 | 20% | 14% | |

| Water | 5 | 7% | 5% | |

| Waste | 5 | 7% | 5% | |

| Stakeholder Engagement | 15 | 21% | 15% | |

| Total | 70 | 100% | 70% |

The GRESB Real Estate Standing Investments Benchmark consists of participants completing both the Management and Performance Components. The GRESB Development Benchmark consists of participants completing both the Management and Development Components. While each Component determines an individual score (ie: Management Component Score, Performance Component Score, Development Component Score), the GRESB Scores and GRESB Ratings only apply to entities completing all relevant Components for their portfolios. The possible combinations are set out below and illustrated in the diagram that follows:

A: Portfolios with only standing investments submit:

B: Portfolios with only development projects submit:

C: Portfolios with both standing investments and development projects submit:

The detailed scoring methodology as applied to each indicator can be accessed by participants via the Assessment Portal on April 1, 2024. This is shared for information purposes in an effort to increase transparency around the Assessment, Methodology and Scoring processes. GRESB reserves the right to make edits to this document during the scoring and analysis period preceding the 2024 results launch.

The GRESB Rating is an overall measure of how well ESG issues are integrated into the management and practices of companies and funds. The rating is based on the GRESB Real Estate Score and its quintile position relative to the GRESB universe, with annual calibration of the model. It is calculated relative to the global performance of all reporting entities - property type and geography are not taken into account. In this way the GRESB Rating provides investors with insight into the differentiation of overall ESG performance within the global property sector. If certain regions systematically perform better, they will on average have higher-rated companies and funds. If the entity is placed in the top quintile, it will have a GRESB 5-star rating; if it is in the bottom quintile, it will have a GRESB 1-star rating, etc.

Entities with more than 15 points (or 50%) in Management and 35 points (or 50%) in Performance OR 15 points (or 50%) in Management and 35 (or 50%) points in Development will receive the Green Star designation, highlighted through a distinctive markup in the Scorecard and Benchmark Reports.

A pre-set threshold determines an entity’s geographic location and property type:

Each participant is assigned to a peer group, based on the entity’s legal structure (public/private), property type and geographical location. To ensure participant anonymity, GRESB will only create a peer group if there is a minimum of six peers in the group.

Peer group assignments do not affect a company/fund’s score, but determine how GRESB places an Assessment participant’s results into context.

The goal of the peer group creation process is to compare participants who share as many characteristics as possible, while:

Each participant can be part of multiple peer groups, but can only have one active peer group. The active peer group is displayed in the participant’s Benchmark Report. This means that participant A can be in the active peer group of participant B, without participant B being in the active peer group of participant A. The practical consequence of this is that A will be displayed in the Benchmark Report of B under “Peer Group Constituents”, while B will not be displayed in the Benchmark Report of A.

The peer group composition is determined by a simple set of quantitative rules and provides consistent treatment for all participants. If the peer group is too small or has too many participants with the same fund manager, we eliminate filters until we have a valid peer group. There are two ways in which the filter can be widened:

The system attempts to find the best peer group based on the criteria presented above.

Since 2023, GRESB real estate participants have access to a “Customize Peer Group” functionality in the GRESB Portal. This feature allows participants to either confirm their predefined peer group, as allocated by GRESB, or submit edits to the peer grouping criteria.

After the assessment deadline, participants can review their predefined peer group and choose to either confirm or customize it by selecting other characteristics deemed relevant.

For further details such as the Step-by-step guide on how to review your predefined peer group and how to customize peer group please visit the new “Customize Peer Group” functionality.

For public companies, the entity name of the peer group constituents is disclosed in the Benchmark Report. For private entities, only the fund manager’s name of the peer group constituents is disclosed. GRESB provides an opt-in option that discloses the entity’s name (listed) or fund manager’s name (private), as well as the scores for the two components (Management + Performance or Management + Development). However, this is only disclosed to participants in the peer group who also opted to disclose their names and component scores.

Data validation is an important part of GRESB’s annual benchmarking process. The purpose of data validation is to encourage best practices in data collection and reporting. It provides the basis for GRESB’s continued efforts to provide investment-grade data to its investor members.

GRESB validation is a check on the existence, accuracy, and logic of data submitted through the GRESB Assessments. The validation process includes both automatic and manual validation.

Automatic validation is integrated into the portal as participants fill out their Assessments, and consists of errors and warnings displayed in the portal to ensure that Assessment submissions are complete and accurate.

Manual validation takes place after submission and consists of document and text review to check that the answers provided in Assessment are supported by sufficient evidence. The validation rules and process are set and overseen by GRESB but the validation is performed by our third-party validation provider, SAS.

Sustainable Assurance Services (SAS) provides third-party validation services for GRESB. SAS is an accredited, independent certification body, and its subject matter experts will conduct the independent assessments of self-reported ESG data in the GRESB manual validation process.

In light of transparency requirements towards GRESB Investor Members, GRESB introduced a few years ago the Quality Control Process (QCP). The QCP is an additional data quality validation stream aiming to enforce participants compliance with the GRESB reporting requirements in full, and that data is reported in line with the guidance provided in official GRESB guidance document. The QCP consists of both qualitative and quantitative checks covering various areas of the Assessment. Checks are conducted offline throughout the reporting period and after the official submission deadline (July 1st). Selected participants may be required to provide additional clarification and/or make use of the Review Period to perform necessary amendments to their reported data. In case of non-compliance, GRESB reserves the right to reject the corresponding Component submission.

Participants with questions on individual validation decisions can contact the GRESB Helpdesk.

In 2020, GRESB introduced a new Review Period in the Assessment Cycle to further strengthen the reliability of our Assessments and benchmark results. The Review Period will start on September 2, when preliminary individual GRESB results will be made available to all participants and run for the month. During the Review Period, participants will be able to submit a review request to GRESB using a dedicated form. The final results will be launched to both participants and Investor Members on October 1. Public Results events and other results outputs will be rescheduled to October and November in order to accommodate the September Review Period.

For a complete interpretation of the validation decisions in the Assessment, participants can request a Results Consultation (formerly Results Review). For more information about the Results Consultation, click here.

GRESB requires property companies and funds to report on their whole portfolio, including both Landlord Controlled and Tenant Controlled areas (see below).

The Annual GRESB Assessment includes all assets that are held during the reporting year, including those that have been sold or purchased. For these assets, ESG data is reported for the period of time that the assets were part of the portfolio. This enables us to deliver the standardized and comparable assessment of portfolio-level ESG performance that the market is seeking. However, it is also worth noting that in addition to simple overall scores of ESG performance - such as the GRESB Real Estate Score and GRESB Ratings - we provide detailed aspect-level and individual indicator-level assessments of performance. This richer analysis, further complemented by peer group benchmarking, enables managers to understand their results in the context of their investment strategies and communicate this to their investors.

Joint ventures

GRESB requires property companies and funds to report on their whole portfolio, including both Landlord Controlled and Tenant Controlled areas (see below for specific guidance). Participants must report on all underlying assets in their portfolio, regardless of the percentage of ownership, but excluding vacant land, cash, ground leases or other non-real estate assets owned by the entity.

When an asset is owned as part of a joint venture (JV), joint operation, or is in joint ownership, participants are required to report on these assets, even if the joint arrangement means that the participant does not have direct operational control over the asset(s).

Assets that were owned for only one day during the reporting year should be excluded from the reporting scope.

If an asset is part of multiple portfolios managed by the same fund manager, the asset should be treated as a JV in each portfolio. The rules outlined above apply.

Landlord/Tenant Controlled Areas

In the past, GRESB used to classify assets as Managed or Indirectly Managed. Such classification was based on the notion of operational control and aligned with the GHG Protocol. In 2020, this concept was replaced by "Landlord Controlled" and "Tenant Controlled" areas, where the same notion of operational control applies to differentiate one from the other. However, while the rationale remains unchanged compared to previous years, the distinction now takes place at the space/area level. Consequently, one asset can include both landlord and tenant controlled areas. The definition of Landlord and Tenant Controlled areas in the Assessment is solely based on the landlord/tenant relationship.

Landlord controlled areas are those for which the landlord is determined to have “operational control” where operational control is defined as having the ability to introduce and implement operating policies, health and safety policies, and/or environmental policies. If both the landlord and tenant have the authority to introduce and implement any or all of the policies mentioned above, the area should be reported as landlord controlled. Where a single tenant has the greatest authority to introduce and implement operating policies and environmental policies, the tenant should be assumed to have operational control. For example, in the case of a full repairing and insuring (FRI) lease in England and Wales, the tenant has operational control meaning that the area is tenant controlled.

GRESB distinguishes between Landlord and Tenant Controlled areas in the Energy, GHG Emissions, Water, and Waste aspects of the Performance Component. GRESB has done so in recognition of the fact that landlords of tenant controlled areas may have little or no control over the use or purchase of utilities for the asset, or over waste management practices. The guidance for this aspect explains GRESB’s approach in more detail.

GRESB does not specifically distinguish between landlord-and tenant controlled areas outside of the Energy, GHG Emissions, Water, and Waste aspects. The Assessment measures ESG performance using a consistent methodology that applies both to listed companies and private funds and which applies across property sectors and regions. GRESB encourages the collection of data and qualitative information regarding ESG issues that give property companies and funds and their investors the tools to identify areas in which they can improve performance and as a toolkit for internal and external engagement.

Furthermore, while GRESB does measure absolute performance, it emphasizes the importance of peer group comparisons in scoring and the analysis of benchmark results. Where participant numbers allow this, GRESB creates separate peer groups for each property type, for listed and private entities and for Landlord and Tenant Controlled areas. Additionally, participants have the opportunity to explain the composition of their portfolio in the open text box in R1.1, including clarifying limits on asset control that arise from the landlord/tenant relationship.

With these factors in mind, while the landlord’s day-to-day involvement in tenant controlled areas may be limited, the topics covered by the Assessment are equally relevant to landlord controlled areas. Accordingly, the same questions and methodology apply.

This section provides an overview of the 2024 Real Estate Assessment Changes.

The Foundation has recently published its forward-looking 2024 Roadmap, which reflects upon future priorities for the Committees and the Standards for the near- and longer-term future highlighting the key drivers for Standard development and areas of work prioritized for 2023-2024, along with issues under consideration for 2025 and beyond. The High-level considerations that influence GRESB Standard Development include:

For further details on the Foundation’s 2024 Roadmap, see this document.

Following the GRESB Standard Development Process formalized in early 2022, the GRESB Foundation has reviewed and approved changes throughout 2023 aiming to develop, maintain and improve the GRESB Standard. There are four types of changes:

For a full list of the 2024 Real Estate Standard Changes, see Appendix 1.

This section provides an overview of the 2024 Real Estate Standard Changes.

Following the standard development process formalized in early 2022, the GRESB Foundation has reviewed and approved changes throughout 2023 aiming to develop, maintain and improve the GRESB Standard. The complete list of changes related to the 2024 Standard is presented in this document. There are four types of changes:

The Foundation has recently published its forward-looking 2024 Roadmap, which reflects upon future priorities for the Committees and the Standards for the near- and longer-term future highlighting the key drivers for Standard development and areas of work prioritized for 2023-2024, along with issues under consideration for 2025 and beyond.

The High-level considerations that influence GRESB Standard Development include:

| RM5 |

Climate resilience and opportunities (RM5)Background and Purpose: The previous Standard only covered climate-related risks and did not address climate-relate opportunities (CROs). CROs are a critical aspect of the Task Force on Climate-related Financial Disclosures (TCFD) framework. Reflecting both risks and opportunities ultimately allows entities considering future climate scenarios to understand the full potential outcomes of their activities, and to align more closely with the TCFD. The GRESB Foundation recommended the Standard better incorporates CROs to increase alignment with TCFD. During 2023 the inaugural International Sustainability ISSB Standards – IFRS S1 and IFRS S2 – were published. The IFRS S1 and S2 align with and supersede TCFD. By incorporating CROs this year the Standards also align closer to IFRS. IFRS will be reviewed in future years in terms of even closer alignment, rather than TCFD. Additionally, it was identified that the list of available transition and physical climate scenarios required an update to include the new ‘Shared Socioeconomic Pathways’ (SSP). Description of Change: Scope of indicator RM5 Climate resilience is now expanded to cover climate-related opportunities along with textual clarification. The list of physical and transition scenario options is updated to include new SSP scenarios. Scoring Impact: Indicator RM5 is now worth 0.5 points, through a reallocation of scoring weight from existing Risk Management indicators (see Scoring Weight Reallocation Overview below). Reporting Impact: Participants are required to incorporate resilience into their climate strategy and provide a description of how the entity does so in light of any climate-related risks and opportunities. Participants are now able to select the new SSP-RCP pathways if they use them in their Physical and/or Transition Risk scenario analysis. This indicator will not be prefilled in 2024. |

Energy efficiency scoringBackground and Purpose: As part of the Foundation’s continuous work on Net Zero set as the number one priority for development in the GRESB Standard, scoring energy efficiency stands out as a key development opportunity for the 2024 Standard. This change is also in line with the strategic direction of travel for the Standard which is to transition towards better recognizing and scoring operational performance of real estate assets. Considering the complexity of the topic and variety of possible approaches to doing so, the Foundation supports the implementation of a phased approach in the Standard, which will be subject to continuous refinement over time and heavily informed by members’ feedback. Description of Change: Introduction of energy efficiency scoring as a supplemental insight in the Standard. Methodological details relating to the energy efficiency scoring approach include:

Final technical details will be communicated as part of the 2024 GRESB output. Scoring Impact: Although this section is subject to scoring, it will not directly impact the overall GRESB Score in 2024. It will however inform future Standard developments as it transitions towards assessing and scoring actual performance of reporting real estate portfolios. The methodology will be subject to continuous refinements over time and is ultimately expected to be fully integrated into the GRESB scoring model. Reporting Impact: No reporting impact as this section solely relies on existing data points reported by GRESB participants. |

| EN1 |

Separating operational vs non-operational Energy ConsumptionBackground and Purpose: Previously, the Standard did not clearly differentiate between Energy consumed for operational purposes and other types of consumption in indicator EN1 Energy consumption. The GRESB Foundation identified a clearer differentiation between the two as a necessary step to properly calculate energy intensity values, and ultimately score energy performance in the Standard. Description of Change: Introduction of a new asset-level data input field (via the GRESB Portal) aiming to collect other types of Energy consumption (deemed non-operational) separately from Energy consumed for operational purposes. While the scope of this field might be subject to further refinements in the future based on members’ feedback, its initial scope predominantly focuses on EV charging stations as it represents the most common and material type of Energy consumption considered non-operational for a standing asset. Reporting guidance of indicator EN1 is now adapted to ensure that Energy consumed for operational purposes is properly isolated from other types of consumption. Scoring Impact: No scoring impact, energy data reported by participants in this field will not be included in the measurement of operational energy profiles of assets, used for scoring Energy LFL Change metrics. Reporting Impact: If applicable, participants are required to report (via the Asset Portal) EV charging stations' consumption separately from operational energy consumption in indicator EN1. |

| BC1.1/BC1.2/DBC1.2 |

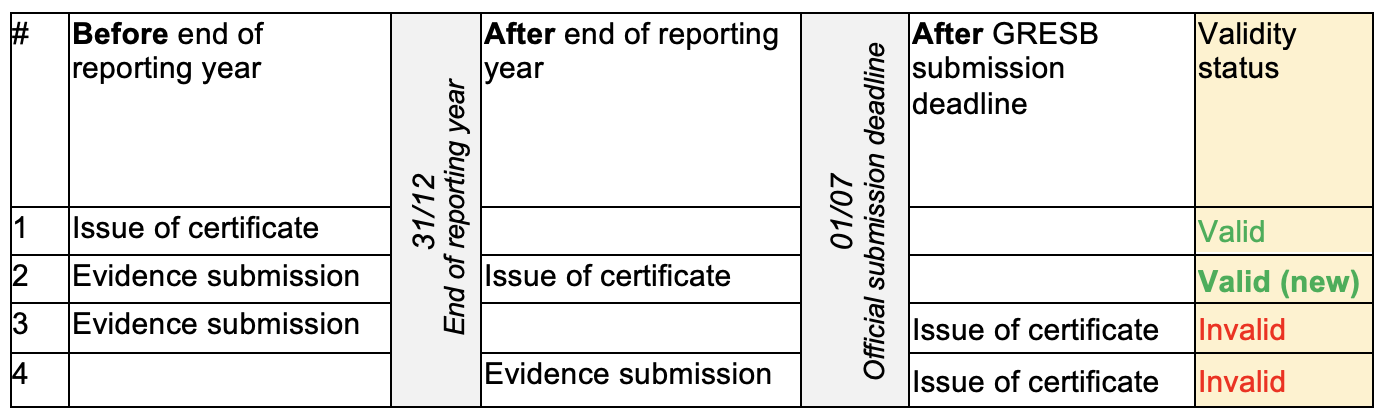

Timing of building certification and validityBackground and Purpose: The validity of a new certification scheme for the reporting year was previously based on the certification issue date. As the certification issue date may differ from the reporting year subject to certification, it can result in a mismatch between the validity period of a certification and the reporting year for which GRESB participants report this certificate. Description of Change: The GRESB guidance for indicators BC1.1, BC1.2 and DBC1.2 is amended to refer to the actual performance or assessment period (reporting period covered by the certification process) as the period determining the validity of a reported scheme. Scoring Impact: No scoring impact. Reporting Impact: Participants are now able to report in indicators BC1.1 and BC1.2 and DBC1.2 building certifications awarded by the certifier after the end of the reporting year if:

Example for an entity reporting on period 01.01-31.12:

|

| BC1.1/BC1.2 |

Building certifications age and expiration yearBackground and Purpose: Building certifications have been identified by the GRESB Foundation as a high importance topic to be progressively better assessed and scored in the Standard. As a first step towards more developments in the future, the Foundation focuses on better considering the evolving relevance of reported building certifications over time, and thereby imposing an expiration year in the 2024 Standard. Description of Change: The GRESB Standard now considers the evolving relevance of reported schemes over time and imposes an expiration year for determining the validity of these schemes in indicators BC1.1 Building certifications at the time of design/construction and BC1.2 Operational building certifications. The 2024 Standard does so on the three main types of Building certifications currently recognized: Design/Construction (BC1.1), Operational (BC1.2) and Interior (BC1.1) certifications. Scoring Impact: Metrics previously subject to scoring in indicators BC1.1 and BC1.2 are now multiplied by a “time factor”, reflective of the evolving relevance of the reported scheme over time, thereby considering the building certification’s age in the scores for those indicators. This time factor is defined for each type of building certification individually:

Reporting Impact: For all building certifications reported to the GRESB Standard, participants are now required to report their corresponding Building Certifications Year in indicators BC1.1 and BC1.2 (through the GRESB Asset Portal), which will be subsequently used in the GRESB scoring model. |

In addition to the general changes described above, a tactical review process for the Standard was initiated in 2023 with as primary purposes of:

This section presents the result of this review process conducted by the GRESB Foundation. While the focus has been predominantly on the Management Component for the 2024 Standard, the intention is to expand its scope to other Components in future years.

Finally, note that since this review is heavily informed by direct user feedback during the reporting year, comments are welcome and can be shared anytime with GRESB via our online helpdesk.

| LE2 |

ESG ObjectivesBackground and Purpose: The Standard previously allowed participants to report General sustainability as well as Environment, Social and Governance-specific objectives in indicator LE2 ESG objectives. Both options fwere considered significantly overlapping with each other. Indicator LE2 previously inquired about the level of integration of the ESG objectives into the overall business strategy. This section was often deemed too subjective or heavily subject to personal interpretation by participants. Description of Change: The “General sustainability” option is removed from the list of existing ESG objectives in indicator LE2. The section on integration into the overall business strategy is also removed. Scoring Impact: The scoring weight from removed options is reallocated to the remaining list of ESG objectives. Overall scoring weight of indicator LE2 remains unchanged. Reporting Impact: Participants are no longer required to report on, nor rewarded for setting General sustainability objectives. Participants will no longer have to report on the level of integration of their ESG objectives into the overall business strategy. |

| LE5 |

ESG, climate-related and/or DEI senior decision maker (LE5)Background and Purpose: Indicator LE5 previously captured the existence of a senior decision-maker for ESG within the organization, and offered Fund/Portfolio manager as an option. Considering that a Fund/Portfolio manager is often the most common role within the reporting organization responsible for ESG, this option was already captured by indicator LE3, resulting in double counting between the two indicators. Description of Change: The “Fund/Portfolio manager” option is removed from the list of senior roles in indicator LE5. Scoring Impact: The Standard no longer rewards participants for reporting Fund/portfolio managers as the entity’s senior decision-maker in indicator LE5, but continues to do so in indicator LE3. Overall scoring weight of indicator LE5 remains unchanged. Reporting Impact: Participants are no longer able to report Fund/Portfolio Manager as a senior decision-maker for their ESG, climate-related, and/or DEI decision-maker in indicator LE5. |

| LE6 |

Personnel ESG performance targetsBackground and Purpose: Indicator The Standard previously inquired about ESG performance targets for personnel having both financial and non-financial consequences in indicator LE6 Personnel ESG performance targets. The concept of a non-financial consequence is deemed to lack strictness, can be subject to personal interpretation and often confuses participants for supporting those in their uploaded evidence. Description of Change: The Standard no longer rewards participants for including ESG factors with non-financial consequences, such as written or verbal recognition, in the annual performance targets of personnel. As such, the “Non-financial consequences” section is removed from indicator LE6. Scoring Impact: The Standard no longer rewards participants for including ESG factors with non-financial consequences, such as written or verbal recognition, in the annual performance targets of personnel. Overall scoring weight of indicator LE6 remains unchanged. Reporting Impact: Participants are no longer required to report on “Non-financial consequences” in indicator LE6. |

| RP1 |

ESG ReportingBackground and Purpose: The GRESB Standard rewards disclosure through several channels for reporting organizations and does so at entity, manager and group level. Reporting behaviour analysis covering uploaded supporting evidence by participants indicates a significant overlap between proposed options in indicator RP1 ESG reporting, in particular “Section in entity reporting to investors”, resulting in double counting and unnecessary reporting burden for participants. Description of Change: The “Section in entity reporting to investors” option is removed from indicator RP1. Scoring Impact: The Standard no longer rewards participants for disclosure through a “Section in entity reporting to investors”. Overall scoring weight of indicator RP1 remains unchanged. Reporting Impact: Participants are no longer required to report on this option nor provide related supporting evidence. |

| RP2.1 |

ESG incident monitoringBackground and Purpose: Recurring organizational misconduct can increase the risk profile of entities as they can translate into reputational, compliance, and financial risks. Having a defined process to monitor potential misconduct and communicate such risks to key stakeholders is necessary to provide investors with transparency about regulatory risks and liabilities. Description of Change: A scoring weight is introduced to indicator RP2.1 ESG incident monitoring to incentivize entities to have in place a process to monitor potential misconduct and to communicate risks to key stakeholders. In addition, the reference to ESG as a type of misconduct is removed on the basis that any responsible business misconduct can be deemed ESG-related, further aligning with other global reporting standards. Scoring Impact: A scoring weight of 0.25 points is introduced to indicator RP2.1, broken down according to the relevance of stakeholder types. Reporting Impact: Participants are now rewarded in indicator RP2.1 for having a process to monitor controversies, misconducts, etc. and communicate to key stakeholders. |

| RM1 |

Environmental Management SystemBackground and Purpose: Environmental Management Systems (EMS) that are certified or aligned with a standard provide assurance that environmental impacts are measured and acted upon using a recognized and proven methodology. Previous scoring weight allocation of indicator RM1 Environmental Management System did not properly reward participants for making additional efforts by undergoing alignment or certification process for their EMS. Description of Change: The scoring allocation of indicator RM1 is revised to better recognize Environmental Management Systems (EMS) that are aligned or certified with a standard. Scoring Impact: Participants no longer benefit from having an EMS that is neither aligned nor certified with a standard in indicator RM1. In addition, the scoring weight of indicator RM1 is reduced by 0.25 points reflecting the reallocation of points between indicators RP2.1 and RM1 (see Scoring Weight Reallocation Overview section). Reporting Impact: No reporting impact. |

| T1.2 |

Net Zero TargetsBackground and Purpose: In continuity to the introduction of indicator T1.2 Net Zero targets in the 2023 Standard, the GREB Foundation expresses the increasing importance to incentivize the industry to set Net Zero targets as a critical element of a Net Zero strategy and as such, this indicator should have a dedicated score in the 2024 GRESB Standard. Description of Change: Introduction of scoring weight of 1 point to indicator T1.2 from indicators T1.1 (reduced from 2 points to 1 point). Scoring Impact: Participants are now rewarded for demonstrating a Net Zero target in indicator T1.2. Full score for this indicator is achieved irrespective of the characteristics underlying the Net Zero target. Reporting Impact: No reporting impact. |

Property Sub-Type ReclassificationBackground and Purpose: The Standard previously classified Property Sub-Type Medical Office in the Office sector. Based on industry feedback and supported by data analysis, a very significant portion of participants reporting Medical Office assets did not identify with GRESB’s previous definition nor classification, and rather identify with the Healthcare sector. Description of Change: “Medical Office” Property Sub-Type is now reclassified from Office to Healthcare sector in Appendix 3a – Property Types Classification. The definition of Medical Office is now expanded to also include buildings used to provide diagnosis and treatment for medical, dental, or psychiatric outpatient care. Scoring Impact: Limited scoring impact, only affecting the few instances where benchmarked and scored metrics at Property Sub-Type level occur at a higher level (e.g. Property Type or Sector level) due to an insufficient number of observations. Reporting Impact: No reporting impact. Participants reporting Medical Office properties will find this Property Sub-Type under “Healthcare”. |

Scoring Weights Reallocation Overview

|

|||||||||||||||||||||||||||

Similarly to previous sections, the following change was formally approved by the GRESB Foundation to impact the Real Estate Standard. However, in an effort to provide participants with sufficient notice to collect the necessary data points to report to the GRESB assessment, this change is published today but will only impact the Standard as from 2025.

The full list of 2025 Standard Changes will be made available in October 2024.

| SE4 |

Employee safety indicatorsBackground and Purpose: The Standard currently does not require all proposed options in indicator SE4 Employee safety indicators to be selected in order for participants to be fully rewarded. This change aims to raise the bar for participants ion their monitoring activities on safety indicators. Description of Change: The scoring weight allocation of indicator SE4 will be revised so that all four indicators are required to obtain full points. Scoring Impact: The scoring weight assigned to each selection option of indicator SE4 is reduced from 1⁄2 to ¼ of the total indicator’s score. Overall scoring weight of indicator SE4 remains unchanged. Reporting Impact: No reporting impact. |

In addition to the Standard Changes presented above, the following changes have been acknowledged by the GRESB Foundation as not directly impacting the GRESB Standard. In 2024, these changes mainly relate to reporting mechanism improvements, benchmarking methodologies as well as additional unscored GRESB output.

Facilitate new reporting scenarios for large Residential portfoliosBackground and Purpose: In 2023, the GRESB Foundation identified the priority need for the Standard to better cater for Residential Real Estate in the future. As a first phase of a longer-term plan to achieve this purpose, the change impacting the 2024 Standard aims to facilitate the effective reporting of certain scenarios encountered by large Residential portfolios. Description of Change: Expansion of data input field at the asset level (via the GRESB Asset Portal) allowing multiple Energy Ratings to be reported per asset, along with the adaptation of aggregation model (asset to portfolio) to cater for those new scenarios. In addition, reporting guidance (GRESB Asset Spreadsheet) for Energy Ratings, Building Certifications and Construction Year has been clarified. Scoring Impact: No scoring impact. Reporting Impact: Participants are now able to report multiple Energy Ratings per asset, and benefit from additional reporting guidance on the aggregation of Energy Ratings, Building Certifications and Construction Year. |

Introduction of Country in benchmarking methodologyBackground and Purpose: The granularity of the benchmarking logic occurred previously at Property Sub-Type level, irrespective of the geography of the individual assets. The former approach potentially led to disparate profiles to benchmark against. In an effort to increase benchmarking and scoring relevance in the Standard, Country as a geography factor is incorporated into the benchmarking methodology of the 2024 Standard. Description of Change: Country as a geography factor is incorporated for the following performance metrics currently benchmarked and scored. This includes:

Scoring Impact: GRESB participants will benefit from more granular performance benchmarking and scoring, now assigned at Country level. Reporting Impact: Participants are now required to report %GAV per Property Sub-Type at the Country level, through a new table reflecting the combination of previous indicators R1.1 The entity’s standing investments portfolio during the reporting year and R1.2 Countries/states included in the entity’s standing investments portfolio. Same approach applies to indicators DR1.1 Composition of the entity’s development projects portfolio during the reporting year and DR1.2 Countries/states included in the entity’s development projects portfolio covering assets under developments. |

Representativeness of intensity valuesBackground and Purpose: To calculate intensity values of reported assets in the GRESB output, the 2023 Standard previously imposed a full Data Coverage percentage (100%). Description of Change: In an effort to increase the portfolio representativeness of intensity values provided in the GRESB output, the threshold imposed on Data Coverage is revised to >= 75%* Data Coverage. As such, a separate intensity value will be added to the GRESB output in addition to previously calculated intensities in the Energy, GHG, Water and Waste sections. *Correction: in an effort to apply a more conservation methodology in 2024, the Data Coverage threshold of < 50% initially communicated in the 2024 List of Changes was subsequently revised by the GRESB Foundation to>= 75%. Scoring Impact: No scoring impact. Reporting Impact: No reporting impact. |

Introduction of evidence validation for all climate risk indicators (RM6.1-6.4)Background and Purpose: In prior years the GRESB assessment manually validated climate risk indicators through the use of an open text box where participants would describe the methodology for identifying transition and physical risks as well as respective impact assessments. However, validating the open text box was deemed inadequate to thoroughly ascertain the intricacies of the process. Description of Change: Evidence of all climate risk indicators are now part of manual validation. Scoring Impact: The evidence is manually validated and acts as a score multiplier. It is assigned a status of “Accepted”, “Partially accepted” or “Rejected”. Reporting Impact: No reporting impact. Participants were required to provide evidence for all climate risk indicators. |

EC1

Reporting entity

Entity name: ____________

Fund Manager Organization Name (if applicable): ____________

EC2

Nature of ownership

Public (listed on a Stock Exchange) entity

Specify ISIN: ____________

Legal status:

Property company

Real Estate Investment Trust (REIT)

Private (non-listed) entity

Investment style:

Core

Value-added

Opportunistic

Debt

Social/Affordable Housing

Open or closed end:

Open end

Closed end

Type of investment vehicle:

Club Deal

Direct Investment

Fund

Joint Venture (JV)

Separate Account

Special Purpose Vehicle

Government entity

Legal Entity Identifier (optional): ____________

EC3

Entity commencement date

![[Year]](/images/tables/year/y2024-7140a687.svg)

EC4

Reporting year

Calendar year

Fiscal year

Specify the starting month Month

RC1

Reporting currency

Values are reported in: Currency

RC2

Economic size

What was the gross asset value (GAV) of the portfolio at the end of the reporting year in millions?

________________________

RC3

Floor area metrics

Metrics are reported in:

m2

sq. ft.

RC4

Property type and Geography

Portfolio predominant location (*): Location

Portfolio predominant property type (**): Property type

RC5

Nature of entity's business

The entity's core business:

Management of standing investments only (continue with Management and Performance Components)

Management of standing investments and development of new construction and major renovation projects (continue with Management, Performance, and Development Components)

Development of new construction and major renovation projects (continue with Management and Development Components)

Management: Leadership

Management: LeadershipLE1

ESG leadership commitments

Has the entity made a public commitment to ESG leadership standards and/or principles?

Yes

Select all commitments included (multiple answers possible)

General ESG commitments

Global Investor Coalition on Climate Change (including AIGCC, Ceres, IGCC, IIGCC)

International Labour Organization (ILO) Standards

Montreal Pledge

OECD - Guidelines for multinational enterprises

PRI signatory

RE 100

Science Based Targets initiative

Task Force on Climate-related Financial Disclosures (TCFD)

UN Environment Programme Finance Initiative

UN Global Compact

UN Sustainable Development Goals

Other: ____________

Provide applicable hyperlink

URL____________

Indicate where in the evidence the relevant information can be found____

Net Zero commitments

BBP Climate Commitment

Net Zero Asset Managers initiative: Net Zero Asset Managers Commitment

PAII Net Zero Asset Owner Commitment

Science Based Targets initiative: Net Zero Standard commitment

The Climate Pledge

Transform to Net Zero

ULI Greenprint Net Zero Carbon Operations Goal

UN-convened Net-Zero Asset Owner Alliance

UNFCCC Climate Neutral Now Pledge

WorldGBC Net Zero Carbon Buildings Commitment

Other: ____________

Provide applicable hyperlink

URL____________

Indicate where in the evidence the relevant information can be found____

No

LE1

Not scored , G

LE2

ESG objectives

Does the entity have ESG objectives?

Yes

The objectives relate to (multiple answers possible)

General objectives

Environment

Social

Governance

Issue-specific objectives

Diversity, Equity, and Inclusion (DEI)

Health and well-being

The objectives are

Publicly available

Provide applicable hyperlink

URL____________

Indicate where in the evidence the relevant information can be found____

Not publicly available

Communicate the objectives and explain how they are integrated into the overall business strategy (maximum 250 words)

________________________

No

LE2

1 point , G

LE3

Individual responsible for ESG, climate-related, and/or DEI objectives

Does the entity have one or more persons responsible for implementing ESG, climate-related, and/or DEI objectives?

Yes

ESG

Select the persons responsible (multiple answers possible)

Dedicated employee(s) for whom ESG is the core responsibility

Provide the details for the most senior of these employees

Name: ____________

Job title: ____________

Employee(s) for whom ESG is among their responsibilities

Provide the details for the most senior of these employees

Name: ____________

Job title: ____________

External consultants/manager

Name of the main contact: ____________

Job title: ____________

Investment partners (co-investors/JV partners)

Name of the main contact: ____________

Job title: ____________

Climate-related risks and opportunities

Select the persons responsible (multiple answers possible)

Dedicated employee(s) for whom climate-related issues are core responsibilities

Provide the details for the most senior of these employees

Name: ____________

Job title: ____________

Employee(s) for whom climate-related issues are among their responsibilities

Provide the details for the most senior of these employees

Name: ____________

Job title: ____________

External consultants/manager

Name of the main contact: ____________

Job title: ____________

Investment partners (co-investors/JV partners)

Name of the main contact: ____________

Job title: ____________

Diversity, Equity, and Inclusion (DEI)

Select the persons responsible (multiple answers possible)

Dedicated employee for whom DEI is the core responsibility

Provide the details for the most senior of these employees:

Name: ____________

Job title: ____________

Employee for whom DEI is among their responsibilities

Provide the details for the most senior of these employees:

Name: ____________

Job title: ____________

External consultant/manager

Name of the main contact: ____________

Job title: ____________

Investment partners (co-investors/JV partners)

Name of the main contact: ____________

Job title: ____________

No

LE3

2 points , G

LE4

ESG taskforce/committee

Does the entity have an ESG taskforce or committee?

Yes

Select the members of this taskforce or committee (multiple answers possible)

Board of Directors

C-suite level staff/Senior management

Investment Committee

Fund/portfolio managers

Asset managers

ESG portfolio manager

Investment analysts

Dedicated staff on ESG issues

External managers or service providers

Investor relations

Other: ____________

No

LE4

1 point , G

LE5

ESG, climate-related and/or DEI senior decision maker

Does the entity have a senior decision-maker accountable for ESG, climate-related, and/or DEI issues?

Yes

ESG

Provide the details for the most senior decision-maker on ESG issues

Name: ____________

Job title: ____________

The individual’s most senior role is as part of

Board of Directors

C-suite level staff/Senior management

Investment Committee

Other: ____________

Climate-related risks and opportunities

Provide the details for the most senior decision-maker on climate-related issues

Name: ____________

Job title: ____________

The individual’s most senior role is as part of

Board of Directors

C-suite level staff/Senior management

Investment Committee

Other: ____________

Diversity, Equity, and Inclusion (DEI)

Provide the details for the most senior decision-maker on DEI:

Name: ____________

Job title: ____________

The individual's most senior role is as part of:

Board of directors

C-suite level staff/Senior management

Investment committee

Other: ____________

Describe the process of informing the most senior decision-maker on the ESG, climate-related, and DEI performance of the entity (maximum 250 words)

________________________

No

LE5

1 point , G

LE6

Personnel ESG performance targets

Does the entity include ESG factors in the annual performance targets of personnel?

Yes

Does performance on these targets have predetermined financial consequences?

Yes

Select the personnel to whom these factors apply (multiple answers possible):

Board of Directors

C-suite level staff/Senior management

Investment Committee

Fund/portfolio managers

Asset managers

ESG portfolio manager

Investment analysts

Dedicated staff on ESG issues

External managers or service providers

Investor relations

Other: ____________

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

No

No

LE6

2 points , G

Management: Policies

Management: PoliciesPO1

Policy on environmental issues

Does the entity have a policy/policies on environmental issues?

Yes

Select all environmental issues included (multiple answers possible)

Biodiversity and habitat

Climate/climate change adaptation

Energy consumption

Greenhouse gas emissions

Indoor environmental quality

Material sourcing

Pollution prevention

Renewable energy

Resilience to catastrophe/disaster

Sustainable procurement

Waste management

Water consumption

Other: ____________

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

Does the entity have a policy to address Net Zero?

Yes

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

No

No

PO1

1.5 points , G

PO2

Policy on social issues

Does the entity have a policy/policies on social issues?

Yes

Select all social issues included (multiple answers possible)

Child labor

Community development

Customer satisfaction

Employee engagement

Employee health & well-being

Employee remuneration

Forced or compulsory labor

Freedom of association

Health and safety: community

Health and safety: contractors

Health and safety: employees

Health and safety: tenants/customers

Human rights

Diversity, Equity, and Inclusion

Labor standards and working conditions

Social enterprise partnering

Stakeholder relations

Other: ____________

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

No

PO2

1.5 points , G

PO3

Policy on governance issues

Does the entity have a policy/policies on governance issues?

Yes

Select all governance issues included (multiple answers possible)

Bribery and corruption

Cybersecurity

Data protection and privacy

Executive compensation

Fiduciary duty

Fraud

Political contributions

Shareholder rights

Other: ____________

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

No

PO3

1.5 points , G

Management: Reporting

Management: ReportingRP1

ESG reporting

Does the entity disclose its ESG actions and/or performance?

Yes

Please select all applicable options (multiple answers possible)

Section in Annual Report

Select the applicable reporting level

Entity

Investment manager

Group

Aligned with Guideline name

Disclosure is third-party reviewed:

Yes

Externally checked

Externally verified

using Scheme name

Externally assured

using Scheme name

No

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

Stand-alone sustainability report(s)

Select the applicable reporting level

Entity

Investment manager

Group

Aligned with Guideline name

Disclosure is third-party reviewed:

Yes

Externally checked

Externally verified

using Scheme name

Externally assured

using Scheme name

No

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

Integrated Report

*Integrated Report must be aligned with IIRC framework

Select the applicable reporting level

Entity

Investment manager

Group

Disclosure is third-party reviewed:

Yes

Externally checked

Externally verified

using Scheme name

Externally assured

using Scheme name

No

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

Dedicated section on corporate website

Select the applicable reporting level

Entity

Investment manager

Group

URL____________

Indicate where in the evidence the relevant information can be found____

Other: ____________

Select the applicable reporting level

Entity

Investment manager

Group

Aligned with Guideline name

Disclosure is third-party reviewed:

Yes

Externally checked

Externally verified

using Scheme name

Externally assured

using Scheme name

No

Provide applicable evidence

or URL____________

Indicate where in the evidence the relevant information can be found____

No

RP1

3.5 points , G

RP2.1

Incident monitoring

Does the entity have a process to monitor controversies, misconduct, penalties, incidents, accidents, or breaches against the codes of conduct/ethics?

Yes

The process includes external communication of controversies, misconduct, penalties, incidents or accidents to:

Clients/Customers

Community/Public

Contractors

Employees

Investors/Shareholders

Regulators/Government

Special interest groups (NGOs, Trade Unions, etc)

Suppliers

Other stakeholders: ____________

Describe the process (maximum 250 words): ____________

No

* The information in RP2.1 and RP2.2 may be used as criteria for the recognition of Sector Leaders.

RP2.1

0.25 points , G

RP2.2

ESG incident occurrences

Has the entity been involved in any ESG-related breaches that resulted in fines or penalties during the reporting year?

Yes

Specify the total number of cases which occurred: ____________

Specify the total value of fines and/or penalties incurred: ____________

Specify the total number of currently pending investigations: ____________

Provide additional context for the response (maximum 250 words)

________________________

No

* The information in RP2.1 and RP2.2 may be used as criteria for the recognition of Sector Leaders.

RP2.2

Not scored , G

Management: Risk Management

Management: Risk ManagementRM1